Why Democratic Presidents Are Better for the Economy

The Pitch: Economic Update for April 4th, 2024

Friends,

This week, the Economic Policy Institute issued a report that looks deeply into the economic records of American presidents from 1949 to the present, and it came to some interesting conclusions. On every single economic metric—from Gross Domestic Product to job growth, the unemployment rate, wage growth, income per capita, inflation, and interest rates—Democratic presidents have outperformed their Republican peers.

What’s more, the report found that the “Democratic advantage is across the board in all variables we measure but strongest in private-sector outcomes—notably, business investment, job growth, and the growth of market-based incomes” and “income growth (adjusted for inflation) was faster on average and far more equal during Democratic administrations, and the Democratic advantage shows up for every group.”

Due to its partisan subject matter this is a report that’s sure to rankle the self-described centrist talking heads on cable TV and social media, so let’s talk about why these findings are important and should be shared. First of all, polling has always shown that the American people consistently believe Republican leaders are better at running the economy than Democrats. And secondly, polling also shows that the American people believe Republicans are better stewards of private enterprise and small businesses than Democrats.

Both of these deeply held assumptions are not only wrong, but completely backwards. The data conclusively show that Democratic presidents produce better results for the economy in general, and for the private sector in particular, than Republican presidents.

EPI concludes that “it is our sense that the simple facts on real-time economic performance during Democratic and Republican administrations—and how starkly better this performance is during Democratic administrations—aren’t particularly well known,” so they consider sharing this report to be “important information people should have during this time of rampant misinformation.”

But as we’ve seen over the last year with lowering inflation numbers and rising frustration over prices among average Americans in economic polls, a fancy set of numbers can’t convince people that their economic standards have improved. And we’ve said many times here in The Pitch that GDP prioritizes the super-rich and corporations over everyone else and so is an unreliable indicator of the economic health of individuals. So, there are plenty of places to legitimately quibble with the details of these findings.

But the wide scope of information behind this study is rock-solid. EPI’s report is largely based on the foundation laid by a non-partisan, peer-reviewed article published in the American Economic Review in 2016. You can see the data in this table:

One thing that neither this EPI article nor the original American Economic Review report really get into is an explanation for why this is the case. After all, EPI notes that “The president does not have total control over the economy, and there is a lot of luck and chance that determine economic outcomes.”

If I had to guess, I’d say that even though presidents on both sides of the aisle over the last 40 years have been captured by the same neoliberal economic worldview, mistakenly favoring tax cuts for the rich and deregulation as engines of economic growth, the policies of Democratic presidents have still leaned closer to the middle-out end of the spectrum than Republican presidents. Middle-out economics understands that inclusion is the key to economic growth—the more people participate in an economy, the healthier that economy is. Democrats in the trickle-down era still tended to pursue inclusion more in their policy goals, even though they mistakenly believed that inclusion was a trade-off with economic growth.

While Bill Clinton slashed social safety net programs, for instance, he also increased the child tax credit and Earned Income Tax Credit, which served as basic poverty reduction programs, and so poverty decreased by 17 percent over the course of his presidency, and more people were economically empowered to participate in the economy. By contrast, poverty rose under George H.W. Bush before him and George W. Bush after him, and so more people were removed from the economy.

So even though Democratic presidents bought into the trickle-down fiction that CEOs and the super-rich were the real job creators in the economy, they still put enough investments into labor protections and anti-poverty programs that the real job creators—working Americans—were able to create prosperity by spending in their local communities. Now that we see what Democratic presidents can accomplish with the economic version of one hand tied behind their backs, imagine what their economic accomplishments will look like now that we understand how the economy really grows—from the middle out and the bottom up.

The Latest Economic News and Updates

“Almost No Progress” in Reducing Global Poverty Since the Pandemic

Chase Peterson-Withorn, the wealth editor for Forbes magazine—I swear I’m not making that job title up—recently announced that 2024 is “an amazing year for the world’s richest people, with more billionaires around the world than ever before.” Peterson-Withorn is referring to recent data determining that there are 2781 billionaires in the world this year so far—141 more than in 2023.

Rupert Neate, the wealth correspondent for the Guardian—again, his real job title—helped to dimensionalize the size of the global billionaire class’s wealth: “The billionaires are also collectively worth more than ever, with combined assets estimated at $14.2 [trillion] – a $2 [trillion] increase on 2023 and more than the GDP of every country except the US and China.”

While it’s been a spectacular year for the wealthiest .00003% of the global population, the global poor have not fared quite as well. The World Bank’s Data Blog reports that “in 2023, 691 million people (or 8.6% of the global population) are projected to live in extreme poverty (i.e., those living below $2.15/day), which is just below the level prior to the start of the pandemic.” In other words, the World Bank reports, “we have made almost no progress in the fight against poverty since 2019.”

Global poverty levels had actually been dropping precipitously since 1990 thanks to coordinated investments into the very poorest citizens of earth, particularly in China and India, but the pandemic destroyed much of that progress. COVID’s biggest impact was on the global poor, the World Bank reports. “Upper-middle-income and high-income countries experienced declines in poverty in 2020, in large part thanks to the adoption of quick, widespread, and generous social assistance programs,” the authors write.

“Lower-middle-income countries experienced the largest initial setback but went back to pre-COVID poverty rates by 2022,” the World Bank explains. “Low-income countries, by contrast, are still above pre-COVID poverty rates, and are not closing the gap, as they saw poverty increase modestly between 2022 and 2023.”

The global economy is not a vacuum. The increase in the number of billionaires in wealthy countries and the increase in poverty in poor nations are linked. Just as income inequality in the United States has for 40 years tipped in favor of the swelling coffers of the wealthiest 1% by $50 trillion at the expense of everyone else’s paychecks, global poverty is the result of policies that favor a handful of the richest people at the expense of hundreds of millions of people who happened to be born in some of the poorest countries on earth. And just as investing in the working Americans of the middle class is good for the entire American economy, building a strong global middle class would improve the global economy for everyone—from the poorest to the richest.

Who’s Afraid of the Big, Bad Trustbuster?

Jon Stewart, in his new/returning role as Monday host of the Daily Show, interviewed Federal Trade Commission head Lina Khan this week. And in the interview, Stewart himself broke a little news: He admitted that a planned segment with Khan on his short-lived news show on Apple’s streaming TV network Apple TV+ faced interference from the tech giant. Specifically, Stewart told Khan that Apple executives “literally said, ‘please don't talk to her.’”

It’s obvious why Apple would be nervous about hosting an interview with Khan, who has been one of the biggest advocates for breaking up tech monopolies. But it’s a little surprising that they would try to directly intervene with Stewart, who over the last two decades has earned a virtually unmatched reputation in the media for speaking truth to power.

Stewart asked Khan why she thought Apple would interfere with the editorial content of his show. “I think it just shows one of the dangers of what happens when you concentrate so much power and so much decision-making in a small number of companies,” Khan replied. That’s a smart, and diplomatic, answer.

But I think Apple’s successful attempt to scare Stewart off of a Khan profile also shows that even though pundits who cater to the wealthy elites have tried to characterize Khan’s antitrust crusade as “mismanaged” and “whiffing” on substantial matters, the truth is that the wealthy and powerful are terrified that she’s on to something.

What the Media Gets Wrong About California’s New $20 Fast-Food Minimum Wage

This week, as California implements a new law raising the minimum wage of fast-food workers to $20 per hour, I’ve seen a lot of disappointing backsliding in the media. Many of the stories I’ve spotted in the mainstream media about the $20 minimum wage could have come directly from 2011, before the Fight for $15 changed the national conversation for the better.

Over the past week, reporters have basically committed every minimum-wage coverage sin in the trickle-down handbook. They’ve uncritically repeated the claims of business owners that they’ll have to close stores now that the minimum wage has gone into effect. They’ve bought the claim of neoliberal economists that there are “winners and losers” when the minimum wage is increased, and that every minimum wage increase carries with it an increase in job losses.

What most of these stories fail to account for is that none of those claims are true.

While there are always scary headlines promoting anecdotes of businesses closing down whenever the wage goes up, the research shows that businesses don’t close, and in fact many small businesses do better when wages increase. A report from University of Michigan and Carnegie Mellon that was released just two days ago finds that “the average independent business in industries such as restaurants and retail is able to accommodate the minimum wage increases through higher revenues.”

And over 40 years of rock-solid data show that no jobs are lost after minimum-wage increases. The most recent research, in fact, is showing that raising the minimum wage actually creates jobs, which makes sense when you understand that workers spend their bigger paychecks in their communities, creating jobs with their increased consumer demand.

It’s perfectly okay for reporters to talk to business owners at times like these, but it’s necessary to correlate their claims with facts and reality. To repeat those conjectures and threats without repeating the reality of minimum-wage research is journalistic malpractice. And though they try to couch pieces like these as objective journalism, repeating these economic threats without fact-checking them helps wealthy employers intimidate anyone else who might consider raising wages in their own city or state. It’s propaganda, not economics, and should be treated as such.

There’s often a tendency for reporters to treat the latest minimum-wage increase as something out of the ordinary—as the straw that could potentially break the camel’s back. But the truth is that American worker wages have been kept unnaturally low for the past 40 years thanks to trickle-down economics and these wage increases are simply a return to normal. In fact, one economist’s research found in 2022 that had wage growth kept up with worker productivity growth over the past 40 years, the federal minimum wage would already be at $21.50 an hour.

And none of these stories that I’ve seen have mentioned the latest report from the Roosevelt Institute, which shows that California fast food corporations have been running unnaturally high profit margins for a very long time.

It’s a safe bet that many of those outsized profit margins have been extracted from the wages of fast-food workers, who have fallen behind other workers in the restaurant and service industry over time. That’s the real story that reporters should be pursuing.

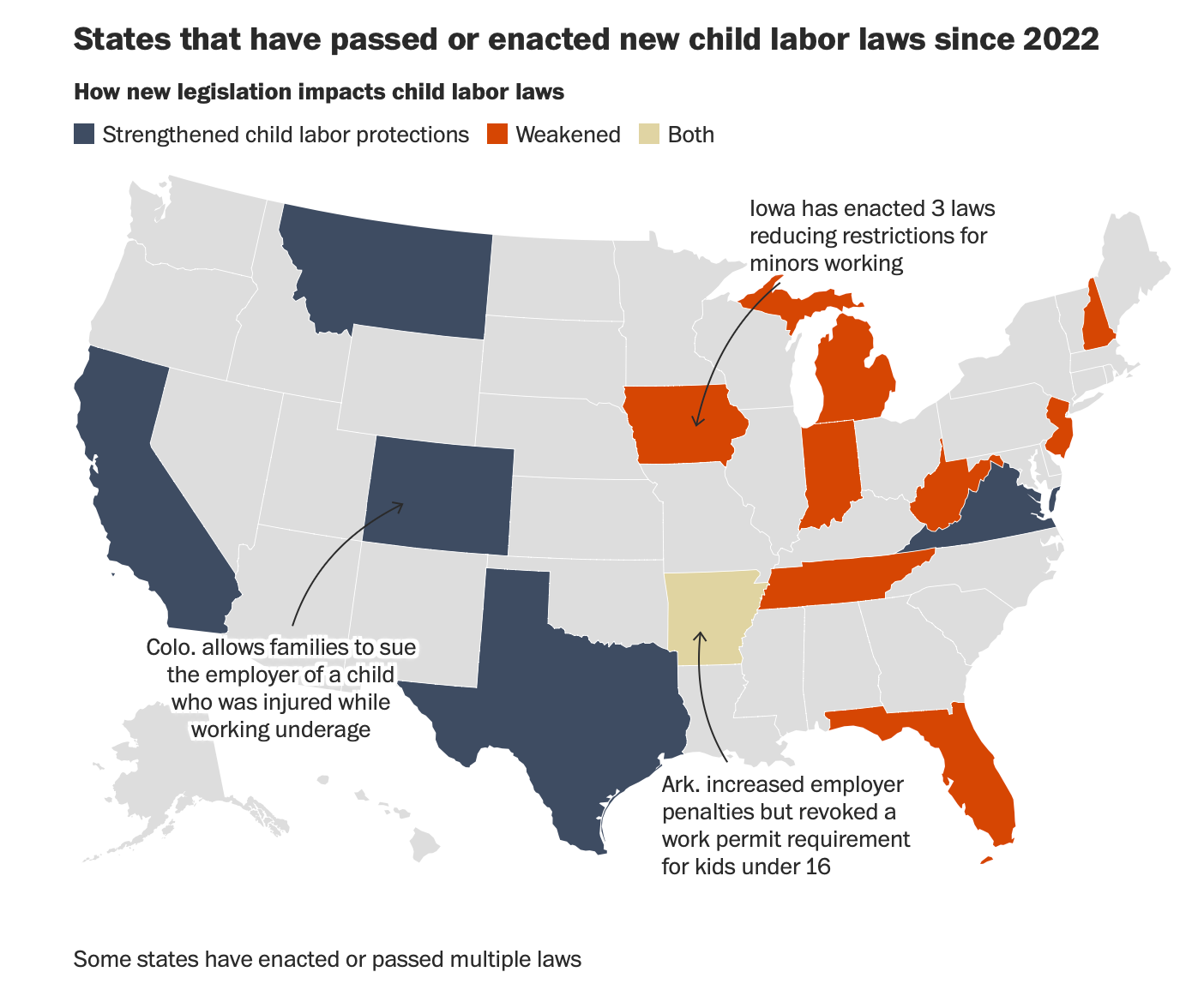

Exploited Workers Are Baked Into the Trickle-Down Plan

Lauren Kaori Gurley at the Washington Post reports that at least 16 states are considering laws to weaken their child labor protections. To her eternal credit, she gets right to the point in the beginning of the piece, identifying the people who are lobbying lawmakers to pass these laws:

“The push for changes to those laws arrives as employers — particularly in restaurants and other service-providing industries — have grappled with labor shortages since the beginning of the pandemic, and hired more teenagers, whose wages are typically lower than adults,” she writes.

Making it easier to exploit cheap labor—and not “teaching kids important lessons about personal responsibility,” as Republican governors have claimed—is the real reason behind this push for relaxing child labor laws. Adult workers are taking advantage of recent wage gains to leave low-paying jobs for better employers, and rather than improve their standards, exploitative employers are trying to find more easily manipulated pools of workers.

We’re also learning that artificial intelligence, which many employers have used as a surveillance tool and a threat to coax workers into accepting lower pay and worse working conditions, is often nothing more than a smokescreen to cover the labor of low-paid workers. The Takeout reports that an AI fast food drive-thru technology called Presto has only added another layer of stress and complexity for the jobs of human drive-thru employees: “Presto’s technology does use AI voice recognition to take down orders in the drive-thru lane, but a significant portion of the process still requires an actual employee’s involvement as well.”

And Gizmodo’s Maxwell Zeff writes about a similar twist to Amazon’s just-shuttered “Just Walk Out” technology, which was promised to eliminate the need for cashiers at grocery and convenience stores. In fact, the technology just allowed Amazon to hire cheaper labor in other countries: “The technology allows customers to skip checkout altogether by scanning a QR code when they enter the store. Though it seemed completely automated, Just Walk Out relied on more than 1,000 people in India watching and labeling videos to ensure accurate checkouts,” Zeff writes.

The AI craze sweeping the business world has prompted CEOs to brag about replacing their human staff with AI—but then they quietly hire even lower-paid workers behind the scenes to do the extra work that the untested, rushed-to-market AI software creates. For many businesses, AI is just another trickle-down tool they can use to intimidate workers into accepting lower wages.

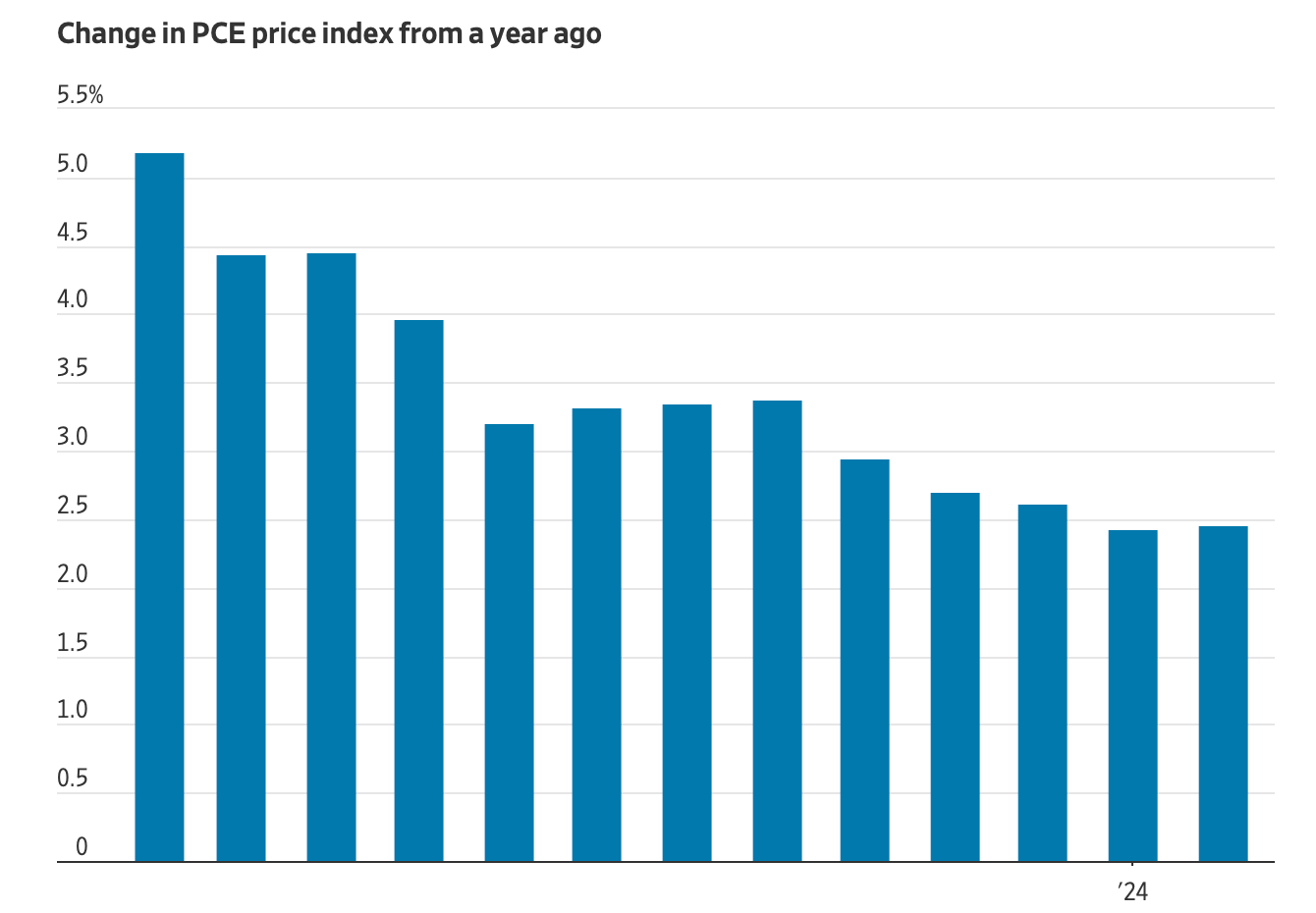

2% Inflation or Bust?

As many experts predicted, the Personal Consumption Expenditure index, which tracks inflation by observing how the prices of a “market basket of goods”impacts consumer spending, rose slightly in February, to 2.5%. Federal Reserve Chair Jerome Powell calmed the economic mainstream by praising the spending report: “It’s good to see something coming in in line with expectations,” Powell announced in a news conference.

That’s good news for people who were concerned that the Fed might keep interest rates high on seeing several inflation metrics stay stubbornly aloft after months of declines. Inflation, both here and around the world, has failed to descend to the Fed’s preferred 2% target, staying a little higher than normal.

It’s worth noting again that the Fed’s favored 2% target rate isn’t based on rigorous economic science. Or, as the Council on Foreign Affairs explains, “The 2 percent target widely adopted by central banks today originated from New Zealand, and surprisingly it came not from any academic study, but rather from an offhand comment during a television interview.”

But quibbling over numbers won’t change the fact that most Americans agree groceries, household supplies, and other necessary items are still too expensive, and occasional shocking price increases are still a part of their everyday experience. So now the Fed is in a holding pattern as they wait to see if this expected lurch in PCE turns out to be a more significant trend, or just another bit of turbulence on the way to a soft landing.

This Week in Middle Out

The Washington Post reports that the Biden Administration has established a new rule that “limits the amount property owners can raise rents if they are part of a tax-credit program for low-income housing. Under new regulations to be announced Monday, yearly rent increases will be capped at 10 percent, according to senior administration officials.”

If you needed yet another report to prove that the enhanced Child Tax Credit was a tremendously useful tool to ease poverty and improve conditions for the poorest American households, the Washington Center for Equitable Growth is happy to help. This report is particularly noteworthy because it directly compares the CTC’s efficacy to the Earned Income Tax Credit, which is a favored poverty-reduction program of neoliberal economists, and explains why the CTC is superior in almost every way.

Peter Coy explores how Intel is navigating the requirements of the Biden Administration’s semiconductor-manufacturing investments and the demands of shareholders. “Subsidies by foreign governments are the main reason it has been 30 percent to 40 percent cheaper to build a fab in Asia, [Intel CEO Pat] Gelsinger said. The share of global chip production capacity in the United States and Europe has fallen to 20 percent from 80 percent over three decades, he said. In words that will be music to Biden’s and Raimondo’s ears, he said, ‘Of course, as the U.S.-born-and-bred R & D, manufacturing and design house, we have a clear bias’ to perform those functions in the United States.”

“The Biden administration on Friday announced a regulation designed to turbocharge sales of electric or other zero-emission heavy vehicles, from school buses to cement mixers, as part of its multifront attack on global warming,” reports the New York Times. “The Environmental Protection Agency projects the new rule could mean that 25 percent of new long-haul trucks, the heaviest on the road, and 40 percent of medium-size trucks, like box trucks and landscaping vehicles, could be nonpolluting by 2032. Today, fewer than 2 percent of new heavy trucks sold in the United States fit that bill.”

The International Monetary Fund argues that the Green New Deal signed into law by President Biden will not be effective unless the Biden Administration does something to speed up the permitting process, allowing green energy companies to come online faster.

The Center for American Progress has put together a neat interactive chart that shows how much money the Medicare drug-price negotiation put into law as part of the Inflation Reduction Act will save individual consumers on a state-by-state basis.

And Vox makes a great case for eliminating a relic of trickle-down social policy that is trapping disabled Americans in a life of poverty: A requirement built into the Supplemental Security Income program that only allows Americans on disability to have $2,000 dollars in financial assets at any time: “in order to qualify for SSI, individual beneficiaries can’t have assets worth over $2,000 and couples can’t have assets over $3,000. And that’s not just checking accounts: it takes things like mutual funds, retirement, and even car values into account. If you go over that limit, you lose that month’s check.” This dumb provision written into the program in the 1970s is in dire need of reform.

This Week on the Pitchfork Economics Podcast

Preston Mui, Senior Economist at Employ America, joins the podcast to discuss his new paper, “The Dream of the 90s is Alive in 2024: How Policy Can Revive Productivity Growth.” In it, Mui explores how the 1990s marked a high-water moment for American productivity. The answer, he explains to Nick and Goldy, is a series of deliberate economic policy decisions. The 1990s weren’t a great decade for income inequality— it’s the period when the trickle-down lessons of Ronald Reagan’s presidency became fully established in every corner of the federal government—but that doesn’t mean we should ignore all the economic lessons that we learned during that time. If we could combine the productivity of the 1990s with the wage growth of the last three years, the American middle class would be virtually unstoppable.

Closing Thoughts

As we often point out in this newsletter, high housing costs are one of the primary contributors to the stubborn increase in inflation numbers. While the standard recommendation is that you should spend no more than 30% of your annual income on rent and/or housing expenses, many Americans are now spending more than 40% of their paychecks on rent or mortgages. While housing rates have spiked virtually everywhere in the country, some places are pricier than others. Phoenix, for example, is now a wildly expensive place to live.

Two weeks ago, we talked about some of President Biden’s proposed fixes for the high price of housing. This week, tax experts are offering their thoughts on how those suggested policies might be improved: “A tax credit for first-time homebuyers could be an important step towards restructuring the way the US subsidizes home ownership,” writes Howard Gleckman at the Tax Policy Center.

“But the version President Biden included in his 2025 budget misses an opportunity by being temporary and by retaining the current mortgage interest deduction (MID),” Gleckman writes, before offering two important tweaks that the Biden Administration should take to heart: “Make the homebuyer credit permanent and repeal the MID, which currently benefits only a small number of mostly high-income homebuyers at a high annual cost.”

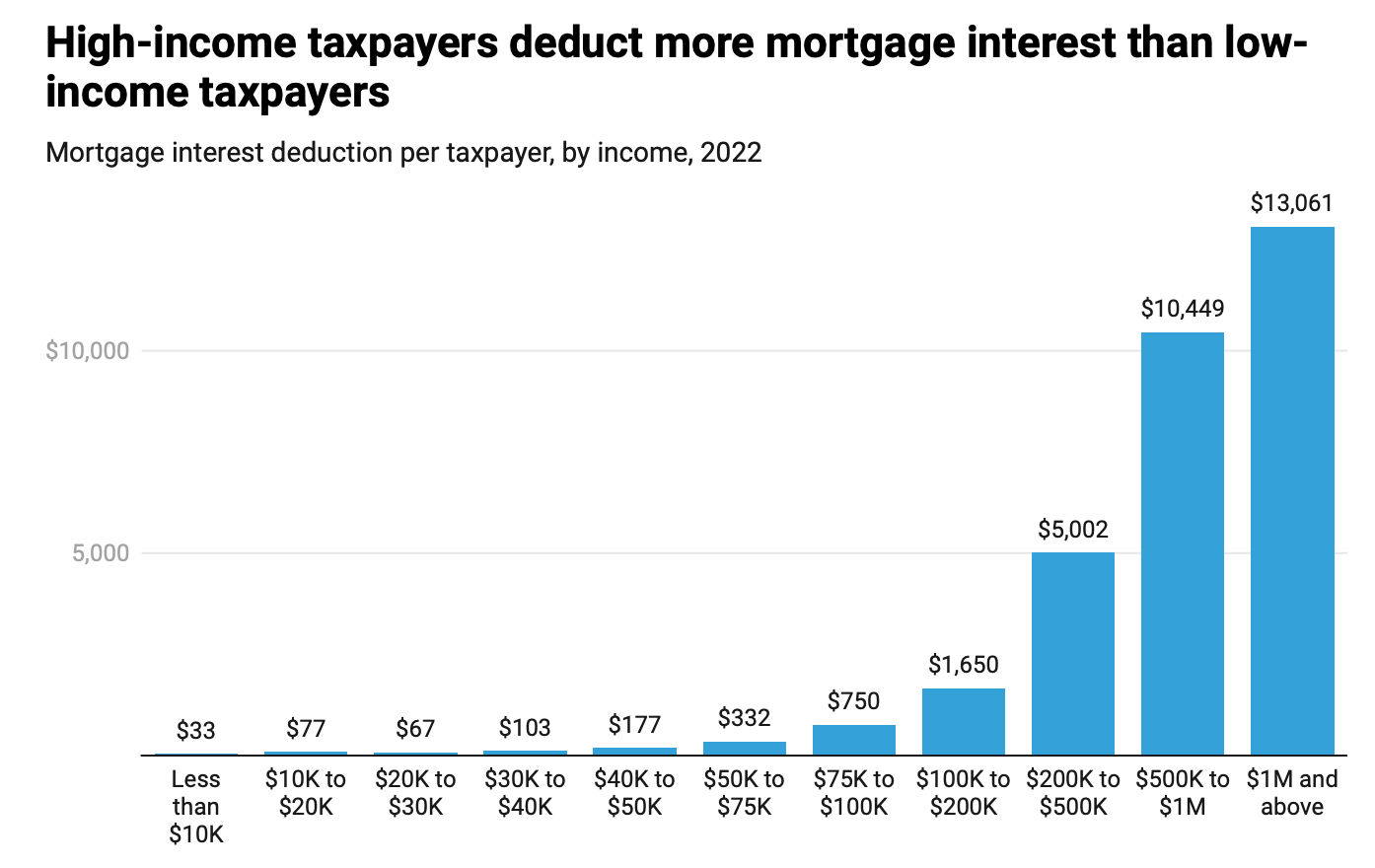

Those are great suggestions—particularly the latter. The mortgage interest deduction allows homeowners to deduct their mortgage interest payments in full from their taxes, and that naturally benefits people who own larger, more expensive homes. Furthermore, there’s no equivalent deduction available for renters, who often are effectively paying off their landlord’s mortgage interest payments.

We need to have a serious conversation in this country about how our tax code privileges wealthy homeowners over renters and people buying more affordable homes. Two years ago, the Center for American Progress wrote about how the mortgage interest deduction is rigged to prioritize wealthy homeowners over everyone else: “The average amount deducted [through the MID] is $13,061 for those with at least a seven-figure income, $2,886 for those with a six-figure income, $274 for those with a five-figure income, and just $33 for those making a four-figure income or less.”

Not only does this deduction favor the wealthy few, it’s also slashing a major potential revenue source for the federal government. In conjunction with a similar tax loophole for the wealthy that allows them to write off their local taxes, the State and Local Tax deduction, CAP found that mortgage interest deductions “reduced government revenues by $50 billion in 2019, with 81.5 percent of that amount—$40.8 billion—going to just the top one-fifth of households. Virtually none of the benefits went to the most disadvantaged Americans.”

Remember, all these acronyms and percentages are in place to intentionally make the tax code confusing and off-putting to Americans who are overwhelmed by attention overload every day of their lives. But if President Biden can communicate just one or two of the ways—like the MID and SALT—in which the tax code enriches the wealthy few at the expense of everyone else, he’d be making a powerful case for unrigging the system for all working Americans.

Be kind. Be brave. Take good care of yourself and your loved ones.

Zach