The War Against Greedflation

The Pitch: Economic Update for September 8th, 2022

Friends,

We at Civic Ventures like to say that in the world of political economy, doing popular things is popular. It might sound glib, but it’s a lesson that many politicians have failed to learn: If you create, pass, and promote policies that benefit the broad majority of the population, you will be more popular. And after decades of elected leaders promoting means-tested and micro-targeted policies to benefit the smallest amount of people possible, Democrats finally seem to be learning the lesson.

This polling presentation from Navigator Research demonstrates what I mean when I say doing popular things is popular: They find that “Majorities find a wide range of Biden’s accomplishments to result in positive outcomes for the country such as the PACT Act, recent job growth, the infrastructure law, declines in gas prices, and gun legislation,” with two in three Americans approving of the Inflation Reduction Act and three in five Americans approving Biden’s move to forgive and reform student debt:

Biden’s favorability numbers have been climbing in recent days. He’s still not above the 50 percent mark, but that’s to be expected in a highly partisan time—the days of 60-percent presidential favorability are, if not gone forever, at least out of reach for now. But despite what pundits tell you, people don’t vote for the candidate with the highest favorability rating. They vote for the candidate that they believe will create the best opportunities for themselves, their family, and their community. This summer of remarkable achievement from Biden and Congressional Democrats has been noticed by Americans, and they overwhelmingly like what they see.

The Latest Economic News and Updates

Greedflation is real

New York Federal Reserve Vice Chair Lael Brainard delivered a speech yesterday about the state of the global inflation crisis. Her speech acknowledges several important points that the Fed has largely ignored over the last few months. Specifically, Brainard addresses the fact that unchecked corporate greed has played a major role in the price increases that Americans are paying.

Brainard notes that “overall retail margins—the difference between the price retailers charge for a good and the price retailers paid for that good—have risen significantly more than the average hourly wage that retailers pay workers to stock shelves and serve customers over the past year,” which indicates that retailers are drawing higher profits than they have in the past, and they’re leaving both consumers and workers to pay the bill.

Ultimately, she concludes, “With gross retail margins amounting to about 30 percent of sales, a reduction in currently elevated margins could make an important contribution to reduced inflation pressures in consumer goods.”

Though Brainard’s message is couched in the bland language of an economist, her message to Wall Street couldn’t be any more clear: Corporate price-gouging has played a major role in rising inflation, and prices will drop and wages will rise once we do something to rein in the profiteering that has benefitted corporations so much this year. New York Times reporter Lydia DePillis framed the speech as an alert about “greedflation,” and that’s a term that deserves to catch on in the mainstream.

In general, this is a great time to be an American worker…

The August jobs report slowed down compared to recent months, but the job market is still much stronger for workers than it was before the pandemic. And the dramatic wage gains we saw over recent months has started to slow down as more workers re-enter the blazing hot job market.

A great New York Times report from Lauren Gurley explores what the situation is like on the ground in one of the hottest job markets in the nation—in Mankato, Minnesota, where the minimum wage is less than $9 an hour but nobody can find workers to scoop ice cream for less than $17. Not every region in the country has seen that kind of growth, but in general this is the best time in over two decades for American workers to switch jobs, with workers who find new employers making an average of 8.5 percent more than workers who stay at their current employer.

Still, the caveat remains that jobs numbers are not equal for all Americans. The Washington Center for Equitable Growth finds that unemployment ticked slightly upward for Black and Latino Americans last month, and the unemployment rate doubles for workers with a high-school diploma or workers who didn’t graduate from high school. And the public sector still has a long way to go to refill the jobs lost during the pandemic:

So the jobs report is mostly good—and far better than where we were two years ago—with lots of room for nuance. Paul Krugman explores that nuance a little further in a recent column, concluding that while prices are too high, “the Biden boom didn’t just increase overall incomes; it reduced inequality,” which means that “so far, Bidenomics has indeed helped workers.”

…But the Fed could wipe out the gains American workers have made

Last week, the Federal Reserve signaled that it was going to continue on its trend of rate increases, making it more expensive to borrow money and slowing down the economy. “The central bank’s campaign is likely to come at a cost to workers and overall growth, [Fed Chair Jerome Powell] acknowledged; but he argued that not acting would allow price increases to become a more permanent feature of the economy and prove even more painful down the road,” writes Jeanna Smialek at the New York Times.

We have an idea of what life would be like for those millions of Americans who could potentially lose work if the Fed continues down this path: Ridiculous amounts of debt, with plenty of new so-called “Pay Later” services ready to exploit needy consumers who need small loans to buy groceries. The problem with those increasingly popular services, writes Priya Krishna at the Times, is that “Some services charge late fees that can exceed the interest charges on credit cards, according to a March report by Consumer Reports. Companies aren’t always transparent about the terms of using the service, and missed payments can hurt users’ credit scores.”

In response, Rakeen Mabud writes at Other Words that “throwing millions out of work would do little to address the root causes of rising prices: outsized corporate power, supply chain shortages, and the war in Ukraine.” She elaborates that our leaders “can’t ‘save’ the economy if people are struggling. After all, we are the economy. When we do well, that’s when our economy thrives.” I couldn’t say it better myself.

Why the Fed shouldn’t be in charge of price stability

And to continue the conversation about the Federal Reserve’s fight against inflation by kicking off massive unemployment, you should definitely read Emily Stewart’s interview with Modern Money Network Research Director Nathan Tankus that was published in Vox today. Tankus argues that the Fed is perpetuating “a scam to say that we need to balance things like inflation on the backs of the unemployed.”

Tankus doesn’t pull any punches in this conversation: “We’ve been sold this lie that we can give this one agency responsibility for managing the economy, inoculated from politics, and then it’ll work out best for everyone,” he says, and he concludes, “We need to take [the Fed’s] ability to try to fix the economy by causing unemployment off the table.”

Tankus believes that rather than giving the Federal Reserve one major lever to raise rates and cause unemployment, government needs to create a “price stability oversight council” that can empower an agency like the Treasury Department to be more proactive with targeted spending.

“That is a way that you can focus on problems before they happen,” Tankus says. “It provides a place for saying, ‘Hey, we need to fix the ports, and we need to do this if we are going to stop inflation.’ There were people in government who were talking about port problems in 2018 and 2019, but no one in government had the foresight to connect this with the inflation conversation.”

It’s never a good thing when institutions perform certain duties simply because that’s the way they’ve always done them. Because the inflation crisis of the 1970s and 1980s eventually ended, our leaders simply assumed that the Federal Reserve acted correctly, and that those same actions would work every time a problem arose. We must consistently interrogate the duties and responsibilities of our government and our financial institutions to ensure that ordinary people aren’t being crushed in the name of sheer institutional momentum. Tankus might not have all the answers, but he asks some very interesting questions that should inspire a much broader conversation.

Union popularity continues to skyrocket

All of the above is a great explanation of why Millennial and Generation Z workers are the most pro-union generations since the high-water mark for American labor in the late 1930s and early 1940s. Harold Meyerson writes for The American Prospect:

According to the 2022 edition of its annual Labor Day poll, Gallup reports that a bare 3 percent of Americans between the ages of 18 and 34 belong to unions. The poll also shows that the percentage of Americans between the ages of 18 and 34 who approve of unions is about 24 times higher than that: 72 percent.

Unions are now popping up in highly unexpected places. Some 4000 cafeteria workers at Google have unionized since the pandemic began, for instance. And in addition, the Washington Post notes that “Tens of thousands more workers voted to join unions in the first half of this year than in the first six months of 2021, according to an analysis by Bloomberg Law. Workers also have voted to unionize for the first time at Chipotle, Trader Joe’s and the recreation equipment maker REI — citing concerns related to safety and low wages.”

Corporations have been fighting back against these unionizing workers using legally questionable tactics. For instance, the NLRB recently filed suit against Starbucks for withholding raises from pro-union employees, and that case is set to go before a judge at the end of October.

Even if you’re not in a union, this push for greater unionization will likely affect you. A new report from the Economic Policy Institute finds that states with higher union density have state minimum wages that are almost 20 percent higher than in low-union-density states. Additionally, states with high union density have higher median household incomes, better unemployment insurance, and better health insurance coverage than the national average. Those are benefits that even non-union workers in those states enjoy.

Those states are also likely to have stronger democracies and paid family and sick leave laws. Taking all this data into account, it’s pretty clear that unions benefit all workers—even workers who haven’t unionized.

What’s at stake in the midterms?

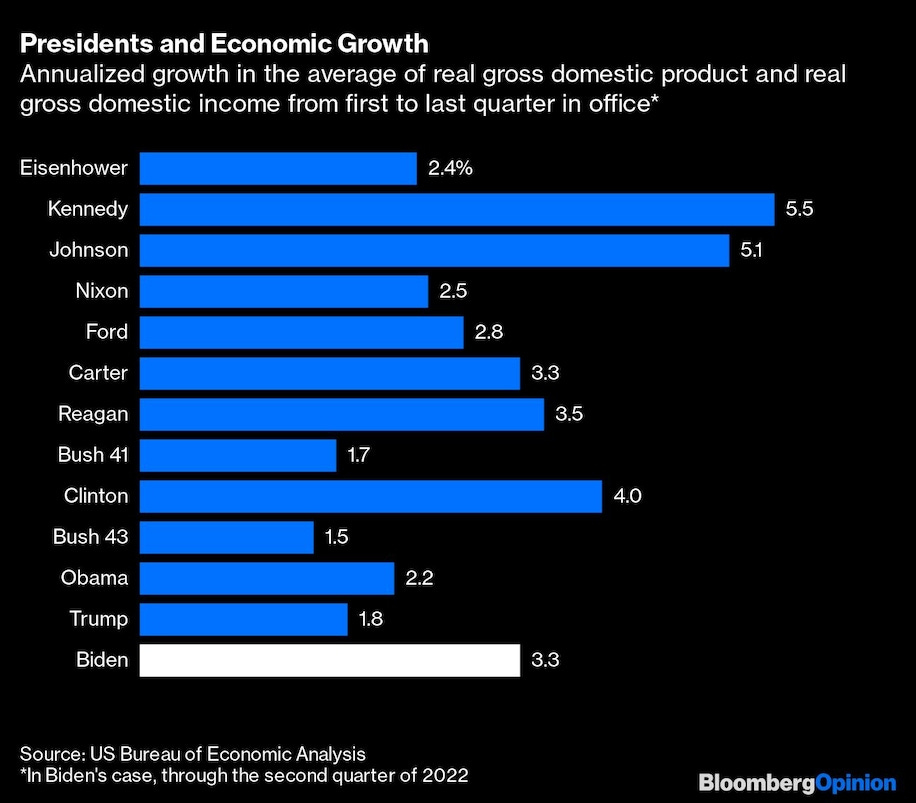

Justin Fox at Bloomberg says that the Biden Administration has the best economic growth record since the Clinton Administration, even when adjusted for inflation:

The caveat to the above chart, of course, is that Biden has only been in office for a little less than two years, and the fate of the next two years of Biden’s term hinges largely on the midterm elections. If Congress swings toward Republican majorities, Biden’s economic agenda could largely be stymied.

Richard Rubin at the Wall Street Journal clarifies what’s on the line in terms of taxes if Republicans regain Congress: Biden’s campaign promises to raise taxes on the wealthy and corporations would fail to come to fruition, and his administration’s attempts to create a global minimum corporate tax would likely collapse.

And the Center for American Progress explains that the entire child care industry is at risk unless Biden fulfills his campaign promises to establish quality affordable childcare. Child care workers simply haven’t been returning to the field as the nation has reopened from lockdowns—largely because other industries are paying more.

As Paul wrote in Business Insider this week, these are the kind of economic policies that Democrats should talk about in the run-up to the midterm elections. By and large, Republicans oppose policies like paid family leave and quality affordable childcare, even though they’re wildly popular with the American people. This provides an opportunity for Democrats to embrace a popular policy and draw a distinction that would make a significant difference in the lives of ordinary Americans. After all, doing popular things is popular.

Real-Time Economic Analysis

Civic Ventures provides regular commentary on our content channels, including analysis of the trickle-down policies that have dramatically expanded inequality over the last 40 years, and explanations of policies that will build a stronger and more inclusive economy. Every week I provide a roundup of some of our work here, but you can also subscribe to our podcast, Pitchfork Economics; sign up for the email list of our political action allies at Civic Action; subscribe to our Medium publication, Civic Skunk Works; and follow us on Twitter and Facebook.

On Civic Action Live this week, we’ll discuss the latest jobs numbers, a New York Fed executive’s stunning speech about “Greedflation,” and the rising popularity of American unions. Join us on Friday morning at 10 am PST.

The Pitchfork Economics podcast returns from summer break with a great interview with economist Rose Khattar about the economic benefits of the Inflation Reduction Act, and how it’s laser-focused on improving economic benefits for the American middle class.

And in his Business Insider column, Paul writes about why Democrat politicians should prioritize policies that benefit women and workers—specifically, paid family leave and quality affordable childcare—as they enter the midterm election season.

Closing Thoughts

Yesterday, Kim Kardashian announced that she was launching a private equity firm. Like any move the Kardashian family makes, the announcement is likely to bring increased media attention to private equity. That might just turn out to be a good thing.

Earlier this year, Mother Jones spotlighted Senator Elizabeth Warren’s long crusade against private equity—or, more specifically, the extractive form of private equity that engages in what Warren calls “legalized looting,” in which scurrilous PE firms buy up struggling brands like Toys R Us and J.C. Penney, saddle them with millions or billions of dollars in debt, and then sell the company for scrap—often laying off tens of thousands of workers in the process. Private equity has also started buying into nursing homes and hospitals, driving up costs and slashing services for millions of the most vulnerable Americans.

Warren and other progressive Congresspeople have introduced common-sense legislation called the Stop Wall Street Looting Act to end PE’s most pernicious behaviors by forcing them to play by the same rules as any other investor: They would be responsible for the losses that their portfolios incur, and they would be required to prioritize payment of workers at firms that they acquire.

But despite Senator Warren’s best efforts, private equity has largely managed to avoid the spotlight, in part because it’s a complicated subject to explain and the media environment is so saturated that it’s hard to get people’s attention. That’s why the Kim Kardashian news is so important: Because it allows organizations like More Perfect Union to use the power of her celebrity to get people’s attention and explain why PE is so terrible for the economy, with the help of another celebrity—the terrific stand-up comedian and professional explainer, Adam Conover:

Politicians have a unique moment here—an opportunity to borrow a celebrity’s spotlight. They can leverage that spotlight to explain how exorbitantly wealthy people rewrite the rules to work in their own favor, at the expense of ordinary Americans everywhere. Maybe all Senator Warren really needed to get the word out about private equity was the unwitting help of a world-famous reality show star.

Be kind. Be brave. Get vaccinated—and don’t forget your booster.

Zach