Friends,

Depending on who you ask, and how you contextualize your question, we are currently living through one of the best economies of our lifetimes, or one of the worst economies of our lifetimes. The signals everywhere are decidedly mixed. Two of the wealthiest people in America, Elon Musk and Jamie Dimon, have warned that they see storm clouds on the economic horizon, even while many Americans have seen remarkable financial success in their own lives. Inflation is pinching our wallets at gas stations and grocery stores, but consumer confidence is nowhere near as low as it was during the Great Recession.

Polling shows that individual Americans are sending mixed economic messages, too: 78 percent of all Americans in an annual household poll report that their household finances are “OK,” a five-year high, but only 24 percent of respondents in the same poll report that the national economy is “good” or “excellent.” Many millions of Americans are enjoying what feels like an economic boom, but at the same time they believe that the economy is ailing and headed in the wrong direction. The economy is like Schrödinger’s cat right now—alive and dead at the same time.

Let’s be clear: Many Americans are suffering. While Axios points out that home values have skyrocketed and retirement funds are flush, millions of people don’t own their own homes, and they don’t have 401Ks to fall back on. The delineation between the haves and have nots still falls clearly across lines of race, gender, and intergenerational poverty, and there’s much work to do to fix the economy so that it works for everyone.

But the fact is that a majority of Americans feel the economy is working for them. That’s why it’s troubling that Federal Reserve Chairman Jerome Powell announced at the end of May that his goal was “to get wages down and then get inflation down without having to slow the economy and have a recession and have unemployment rise materially.”

Respectfully to Mr. Powell, that seems wrong. One credible interpretation of all the above data is that the rising wages of ordinary Americans are the only factor reliably holding the economy aloft. If our economic leadership succeeds in its stated goal to raise unemployment rates and lower wages, the reduced consumer spending brought by slashing the paychecks of ordinary Americans is very likely to tip the economy over into a recession. The middle class powers the economy, and draining its spending power at a precarious moment in history is a terrible idea.

The Latest Economic News and Updates

American workers are still making gains

Lawmakers are taking action to ensure that worker paychecks continue to rise. New York State is considering raising the minimum wage to anywhere from $16.35 to $21.25 (in New York City) by the year 2026. The Economic Policy Institute says the increase would raise wages for 2 million workers around the state. And in Arizona, lawmakers recently pegged the minimum wage to increases in the Consumer Price Index, meaning that if the national inflation rate stays high, workers will get a big raise next year.

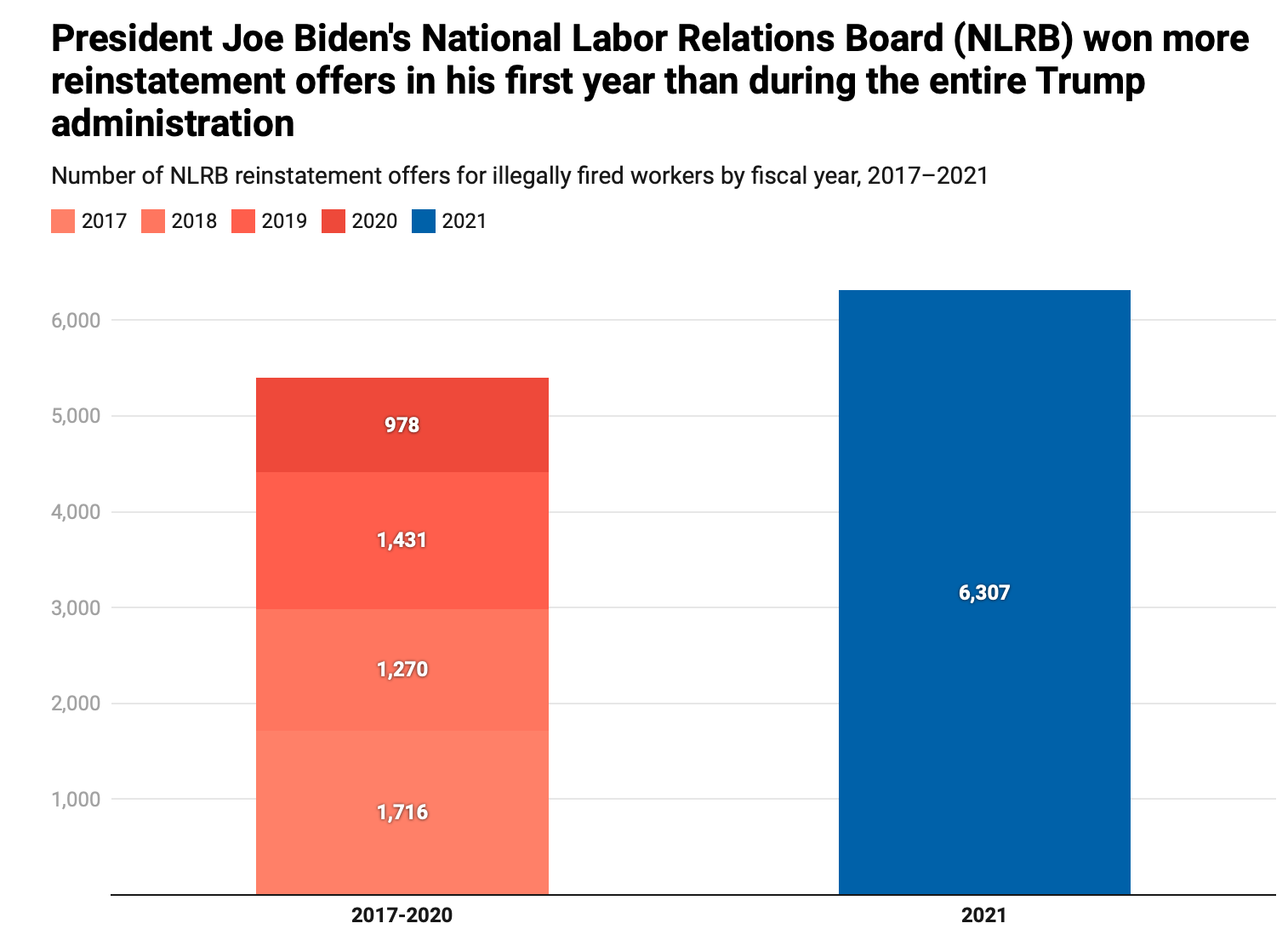

Meanwhile, in Massachusetts, workers at a Trader Joe’s were the first store in the chain to file for a union vote, citing decreased benefits and poor Covid protections. Workers in other Trader Joe’s locations around the country are following close behind the Hadley, Massachusetts store. The Center for American Progress notes that the Biden Administration’s National Labor Relations Board has reinstated more workers who were wrongly fired for union activity in a single year than President Trump’s entire four years in office:

All of these worker gains are creating real-world effects. Bloomberg’s Ben Steverman reports that “America’s Inequality Problem Just Improved for the First Time in a Generation,” with the net worth possessed by the bottom 50 percent of American households (those with a household income of less than $166,000 per year) doubling over the last two years. This is a huge deal!

Steverman is very clear about where these gains come from: They’re “a result of trillions of dollars in Covid-19 relief and a strong labor market that remains hottest for the lowest-income workers.”

There are, of course, a number of caveats. Steverman warns that the racial wealth gap is still huge, with Black workers possessing far less wealth than their white counterparts, and that the wealth earned by the bottom 50 percent is precarious, and growing inflation or a deep recession could erase the past two years’ of gains.

And even if these gains continue, a lot of ground needs to be made up in the battle against wealth inequality. I was especially gobsmacked by the below chart, which shows that a full-time job in America doesn’t guarantee a stable financial status, as compared to the rest of the world. In 2020, nearly a quarter of all full-time workers made less than two-thirds of the median income. That’s because low-quality, extractive jobs in America don’t pay a living wage, and those are the kind of jobs that we have to target if we want to make a significant dent in the wealth gap to improve outcomes for everyone.

On inflation, some promising signs (and a warning)

This week, the World Bank warned of the global threat of 1970s-style “stagflation,” which could kick off a recession in many countries. At the same time, Barry Ritholz at The Big Picture says that inflationary prices in used cars—which, remember, were one of the leading indicators of the most recent wave of inflation last year—have mostly died down, and new car prices are falling too.

Additionally, lumber prices have fallen by more than 50 percent since March, and home prices are falling along with semiconductor, shipping container, and fertilizer prices, all of which were skyrocketing during the early days of the inflation crisis. So while it’s too soon to say whether the numbers will decline, there are some promising signs that inflation might not continue to climb.

The most frustrating thing about the inflation debate is that we’re still not even fully clear about its causes. Treasury Secretary Janet Yellen recently had to argue that pandemic-era spending bills were not a major factor in spiking inflation—an argument that should be obvious, given that other nations which didn’t provide financial support are dealing with inflation of their own. I do recommend Lydia DePillis’s New York Times investigation into the role that corporate consolidation and price-gouging played in the inflation crisis—or, as she puts it, “Greedflation.”

And if you’re the kind of person who likes to argue about economics on social media, you’ll want to bookmark the Economic Policy Institute’s column “Debunking 5 top inflation myths,” which provides handy links that prove higher wages and government support didn’t play a major role in inflation, but that price-gouging did.

The rents are high, but corporate landlord profits are higher

The Washington Post’s Abha Bhattarai reports on the massive rent increases happening in trailer parks around the country, and the nearly 50 percent price increases buyers of mobile homes are paying. Construction prices are high because of inflation, and rent increases are happening all around the country, but also private equity firms are buying up mobile home parks in order to “turn them into more lucrative ventures, including timeshare resorts, wedding venues and condominiums.” While housing costs are hurting pretty much everyone right now, the mobile-home pricing crisis hurts lower-income and elderly Americans even more—the people with the most to lose, with few options left aside from homelessness.

It’s easy to fall into the trickle-down trap of believing that rent increases are the result of some invisible hand, that the market is setting rents just high enough to pay off increased prices. But Irina Ivanova at CBS says that corporate landlords appear to be price-gouging just as much as Big Oil.

“The largest publicly traded property groups in the U.S. saw their combined earnings surge more than 50% last year to nearly $5 billion, government watchdog group Accountable.US found in a new analysis,” Ivanova writes. “During that time, their top executives saw raises of more than 20%, the group calculated.”

In other words, a few greedy executives have decided to take advantage of a crisis situation by raking in outsize profits, with one executive boasting publicly that "tenants seem capable and willing to pay these rent increases," and even calling inflation "an extraordinary gift that keeps on giving."

The pandemic could have lasting effects on lifetime earnings for young workers

The Washington Center for Equitable Growth provides you with the vocabulary word of the day: “hysteresis,” which is defined as the long-term effects of an economic shock. Their latest report examines the long-term effects of economic downturns on young workers just entering the economy. You have no real control over the time you enter the workforce—most people can’t waste a couple years after college to sit tight and wait for the economy to recover before trying to get a job—but the time at which you enter the workforce has huge long-term effects on your lifetime earning potential. You can see here that millennials who sought employment for the first time during the Great Recession are far behind other generations that joined the workforce in more prosperous times:

So what does this mean for young workers entering the workforce right now, in the wake of a global pandemic followed by a strong labor market during a period of high inflation?

As you can probably guess after reading the rest of this issue, the answers are mixed. Students were more likely to graduate high school in 2020 than in other recent years, but college enrollments appear to have declined. Due to the hot job market and higher wages, more teens are taking summer jobs this year than any year since 2007, but entry-level workers were more likely to have lost their jobs during the first year of the pandemic when lockdowns were commonplace.

The Center recommends a few policies to help lessen the impact of hysteresis on this generation of incoming workers, including canceling student loan debt, increased unionization, and, perhaps most intriguingly, a job-seeker’s allowance that would allow people the freedom to not jump at the first job offered to them.

Real-Time Economic Analysis

Civic Ventures provides regular commentary on our content channels, including analysis of the trickle-down policies that have dramatically expanded inequality over the last 40 years, and explanations of policies that will build a stronger and more inclusive economy. Every week I provide a roundup of some of our work here, but you can also subscribe to our podcast, Pitchfork Economics; sign up for the email list of our political action allies at Civic Action; subscribe to our Medium publication, Civic Skunk Works; and follow us on Twitter and Facebook.

On Civic Action Live this week, we’ll be parsing the mixed messages everyone is receiving about both inflation and the economy in general, sharing the amazing advances workers have made in the last month, and talking about what smart cryptocurrency regulation might look like. Join us at 10:30 am PST.

Author Elizabeth Popp Berman joined the Pitchfork Economics podcast to talk to Goldy and I about why lawmakers view every prospective policy strictly through an economic lens, and why cost-efficiency isn’t the best barometer of good policy.

And in his Insider column, Paul explains why inequality isn’t a necessary feature of capitalism, and he identifies the inextricable link between high income inequality and growing political division. Other capitalist nations have decreased income inequality and lowered the temperature on political division, so it is not impossible for America to do the same.

Closing Thoughts

Felix Salmon at Axios reports that in the halls of Congress, leaders are beginning to circle around coherent legislation that will regulate cryptocurrency. If you’ve ever visited the site “Web3 is going just great,” you’ve seen the almost-daily parade of grifts, cons, and outright thefts that crypto customers have experienced over the past year, amounting to hundreds upon hundreds of millions of dollars that have been ripped off from owners of NFTs, crypto, and other digital financial “innovations.”

As we saw with rideshare apps and other gig-economy innovations, technology often moves faster than the law. These “wild-west” periods before legislators take action usually establish a few huge winners and leave a multitude of losers hanging out to dry. In the case of crypto, many small investors who went all-in on digital currency as a way to signal their distaste for the traditional economy have been wiped out, burning money they can’t afford to lose.

The latest proposed legislation co-written by Senators Kirstin Gillibrand and Cynthia Lummis offers a good start for the regulation of crypto, creating definitions for different types of cryptocurrency and establishing requirements for so-called “stablecoins” that protect consumers from total disaster. They also require transparency from crypto creators and navigate a path to tax crypto assets on the state and federal level.

Remember—there’s no such thing as a financial commodity that is free from regulations. As it is right now, crypto is regulated entirely by the people who mint and sell the product, and they’ve rigged the system in their own favor. The result is just as chaotic, inequality-ridden, and dangerous for ordinary consumers as any libertarian pipe dream.

It’s unlikely that the legislation proposed by Gillibrand and Lummis will pass in this exact form. But it’s heartening to see a bipartisan effort to get in front of crypto before it destroys the lives of more ordinary Americans in its current lawless state. This is the latest in a long series of examples that proves why strong, centralized protections are necessary to ensure that everyone has a chance to succeed.

Be kind. Be brave. Get vaccinated—and don’t forget your booster.

Zach