Dancing on the Ceiling

Dancing on the Ceiling

The Pitch: Economic Update for Sep. 30th, 2021

Friends,

I’ll have plenty to say about Congress’s moves this week to pass the Build Back Better plan and bipartisan infrastructure bill, but the most pressing economic issue facing the country for the second week in a row is the Republican refusal to raise the debt ceiling. Congressional Republicans are refusing to raise the ceiling under the pretext that they’re against debt and spending, which is only the case when a Democrat is in the White House. As I wrote last week, if Congress doesn’t raise the debt ceiling, the country could fall into a deep and entirely avoidable recession, with six million jobs lost, trillions in household wealth flushed down the drain, and the pandemic recovery cut off at its knees.

The saddest part of all this is that the debt ceiling drama is entirely manufactured. Our friends at the Economic Policy Institute point out that the debt ceiling isn’t tied to any real economic indicators, and Congress’s raising of the ceiling is entirely ceremonial. In fact, EPI argues, the only true purpose of the debt ceiling is for Congress to force the federal government into austerity measures, cutting spending and investments in everyday Americans.

In fact, EPI notes, the last time the debt ceiling fight played out was in 2011, when a Republican Congress forced the Obama administration to adopt huge budget cuts that slowed the nation’s recovery from the Great Recession and extended 2008’s economic distress for millions of Americans—many of whom are still feeling those effects today. The report calls the Republicans’ 2011 ploy “an anti-stimulus to the U.S. economy about two times as powerful as the stimulus provided by the Obama administration’s Recovery Act in 2009.”

And now Republicans are trying the same play all over again—killing investments in American workers that the Biden administration has already put in place and ensuring that most households will take years to crawl out of the economic distress caused by this pandemic. It’s up to Democrats to resist this power play however they can, and then they should abolish the ceremonial debt ceiling fight so that future generations of Congress won’t have to take part in this manufactured—and hugely damaging—dance on the edge of disaster.

The Latest Economic News and Updates

The pandemic unemployment cliff, visualized

The Hamilton Project has put together a list of 11 facts about the economic recovery. Every item on their list is worth your time, but I wanted to call special attention to item 3, which is about the $300-per-week emergency pandemic unemployment payments that just expired at the beginning of this month.

“We see no compelling evidence that the cancellation of those benefits so far has led to significant increases in aggregate employment,” the paper notes, but “the abrupt elimination of access to UI benefits for millions of people creates financial hardship for those who are unable to work owing to health risks or other constraints.”

The Hamilton Project put together a chart showing the dramatic impact of the sudden cancellation of those $300 weekly checks, and projecting how long that misery will extend for millions of Americans:

If that projected unemployment rate holds true, nearly five million Americans will have to make do for the foreseeable future on either paltry state unemployment insurance payments or with no unemployment payments at all. Through at least the summer of next year, we’re looking at real economic misery for a significant chunk of the United States population.

Looking more deeply at that chart, it’s no coincidence that the biggest dip in unemployment happened when the most money was being invested in the unemployed. That’s because those additional payments were being spent in local economies, driving up consumer demand and encouraging businesses to hire more workers to meet that demand. By slashing the spending power of millions of Americans, our leaders are all but ensuring that the employment rate won’t drastically improve any time soon.

Why Building Back Better is so important—and what’s standing in the way

As I write this, nobody is exactly sure what Congressional Democrats will do with the bipartisan infrastructure bill and the Build Back Better legislation this week. There’s been a boatload of drama, verbal jousting, and blustery speeches, but nobody seems to know if Democrats have enough votes to pass the centerpiece of President Biden’s recovery agenda. This morning’s episode of The Daily includes a good interview with Washington state Congressperson Pramila Jayapal about the stakes of the fight, where the battle lines have been drawn, and what could happen in the days and weeks to come.

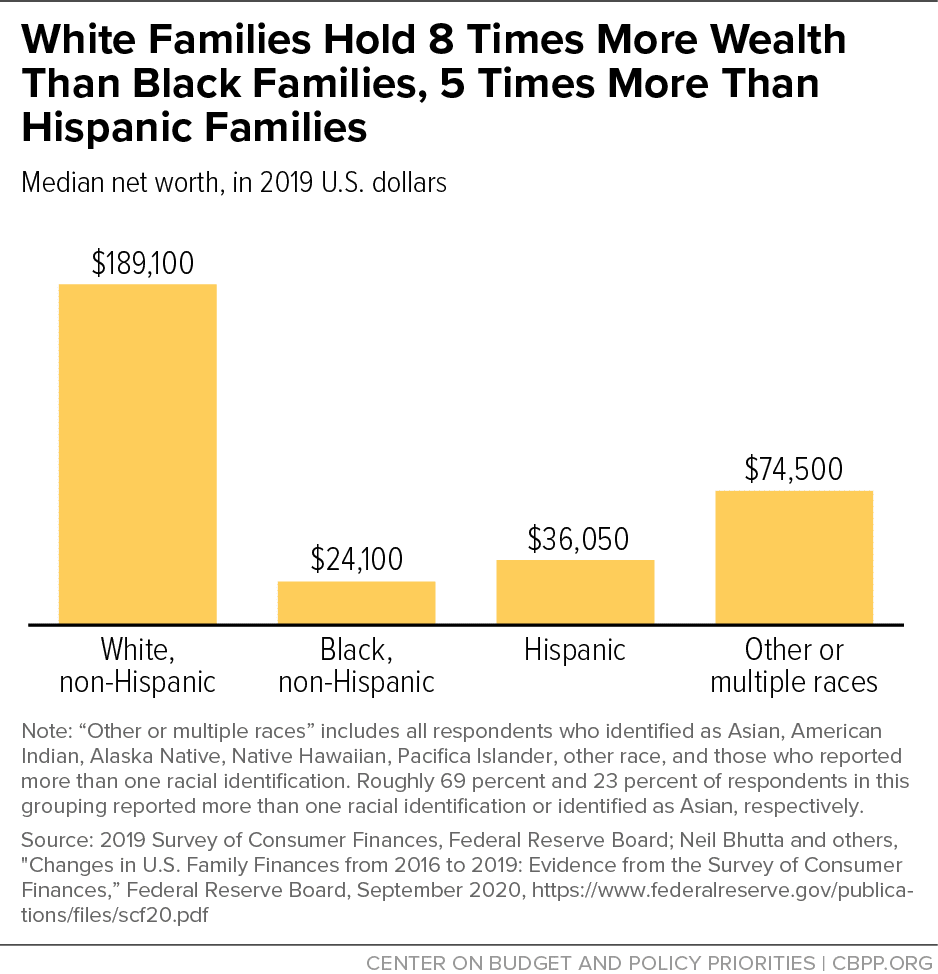

There’s a lot to love about the Build Back Better legislation—it would reduce poverty, increase access to education, fortify the green economy, improve health outcomes, and help address our housing crisis. In a comprehensive new report, the Center on Budget and Policy Priorities points out a hidden benefit of Building Back Better— if it passes, this legislation will hugely advance racial equity in America.

In addition to increasing access to education and housing for nonwhite populations, and shrinking the poverty rate, the Build Back Better plan would also raise taxes on the wealthiest Americans—who are overwhelmingly white. The fact is that we can’t truly create equity in America until household wealth is a lot more even than it is right now:

Meanwhile, Paul Krugman offers an explanation on why so many Congressional Democrats are dragging their feet on the Build Back Better legislation—because they’re what he calls “the Rip Van Winkle Caucus,” committed to the Clinton-era trickle-down theory that all taxation, regulation, and government spending is bad.

“Specifically, some Democrats still seem to believe that they can succeed economically and politically by being Republicans lite,” Krugman writes. “It’s doubtful whether that was ever true. But it’s definitely not true now.”

If Democrats persist in cutting spending and strangling every policy with endless means-testing, they endanger their majority in the House and Senate, and—much more importantly—they risk slowing this economic recovery down to a painful death march like the one we had after the Great Recession.

The most popular government programs—think libraries, Social Security, Medicare—are not means-tested. They’re available to everyone, and virtually everyone agrees that they are important. It’s time for Democrats to let go of the philosophies of the past and embrace the future.

American care workers have been left behind. A $15 minimum wage would help.

It is a national shame that the people who care for our oldest and most vulnerable neighbors are making poverty wages. Last year, we called them “heroes” and labeled their work as “essential,” but direct care workers—those who care for elderly and disabled Americans—are among the lowest-paid workers in America.

EPI finds that raising the federal wage to $15 an hour would benefit almost “2 million direct care workers who provide long-term services and supports.” And since those workers are disproportionately Black, Hispanic, Asian, and Pacific Islander, raising the wage would provide outsize benefits for workers of color. Women, too, would see a huge bump in pay from a national $15 minimum wage:

Those of us who live in high-wage American cities and states tend to think that the $15 minimum wage is a settled issue because it’s been our reality for so long. But there are millions upon millions of workers around the country who would benefit from a $15 federal minimum wage, and we can’t forget about them.

Wall Street’s dirty little secret: Everyone’s doing insider trading

“Most Americans today believe the stock market is rigged, and they’re right,” a professor at the Wharton School tells Bloomberg in a fantastic new story about one of Wall Street’s dirtiest little secrets. Insider trading, which is technically illegal, is happening everywhere, all the time. It’s an open secret that wealthy people—even senators—are using privileged information to profit from stock trades.

The problem, Liam Vaughn writes, is that to convict someone for insider trading, “it’s not enough for prosecutors to simply show that someone profited from nonpublic information; prosecutors have to demonstrate that the defendant knew they had such information and intended to cheat. This helps to make it among the most difficult white-collar crimes to prosecute.”

At a time when information can travel the world almost instantaneously, how can the government reform insider trading laws to un-rig the stock market? One solution proposed by an expert involves a sophisticated computer model that demonstrates how a trader’s portfolio would have performed had they not had access to insider information.

But frustratingly, not everyone agrees that this is a problem worth solving:

Several former government lawyers interviewed for this story questioned how much damage well-timed trading by executives really causes when compared with, say, a Ponzi scheme that takes elderly investors for their savings or an Enron-style accounting fraud that causes a company to collapse when exposed.

Those government lawyers are ignoring the systemic abuses caused by widespread insider trading—perhaps one lone case of trading wouldn’t be worth the resources it takes to prosecute, but if multiple CEOs trade stocks based on secret information, that could easily amount to billions of dollars of wealth transferred to the richest members of society—and when those CEOs go unpunished for their insider trading, more Wall Street types are emboldened to do insider trading of their own.

In order for an economy to work for everyone, there need to be consequences for immoral behavior. Because the wealthy are flagrantly held to a weaker standard than, say, shoplifters at a Walmart, our national sense of trust in the justice system is beginning to unravel—and that’s why the pitchforks that Nick warned about have begun to come out.

Real-Time Economic Analysis

Civic Ventures provides regular commentary on our content channels, including analysis of the trickle-down policies that have dramatically expanded inequality over the last 40 years, and explanations of policies that will build a stronger and more inclusive economy. Every week I provide a roundup of some of our work here, but you can also subscribe to our podcast, Pitchfork Economics; sign up for the email list of our political action allies at Civic Action; subscribe to our Medium publication, Civic Skunk Works; and follow us on Twitter and Facebook.

On Civic Action Live, Jessyn and I will discuss the latest movement (or lack thereof) of the Build Back Better legislation in Congress, the bombshell paper that claims the Fed doesn’t understand inflation, and we’ll take your economics questions live. Join us tomorrow (Friday) morning at 10:30 am on Facebook.

This week, the Pitchfork Economics podcast is re-issuing a favorite episode of mine, about why “Capitalism is working better in Finland.” Authors Anu Partanen and Trevor Corson explain that Nordic countries—which are capitalist, and not socialist as some would have you believe—engage in a much more responsible, thoughtful, and sustainable form of capitalism than the winner-take-all approach we have here in the United States.

And in a special bonus episode of Pitchfork Economics, Communications Workers of America Senior Director Shane Larson explains why right-to-work laws, which make unionizing more difficult, are so terrible for workers. The laws, which have passed in 28 states, result in lower pay, worse workplace conditions, and weakened retirement benefits.

Paul also wrote about right-to-work laws in his Business Insider column: “A large body of evidence proves that as unions continue to lose power, economic inequality grows: CEOs and shareholders take home more profits while worker paychecks shrink.”

Closing Thoughts

Federal Reserve economist Jeremy Rudd published a wonky paper about inflation (PDF) that set off a firestorm in the economics world. Rudd is known as a bit of a bomb-thrower, and the cheeky title of his paper, “Why Do We Think That Inflation Expectations Matter for Inflation? (And Should We?)” offers some hints about where he’s aiming his ire this time.

As Bloomberg explained, Rudd’s paper slams the field of economics for embracing “arrant nonsense” as gospel truth, even though many of those beliefs lack “any sort of empirical foundation.”

Basically, Rudd is calling out economists at the Federal Reserve and elsewhere for using inflation expectations as a guiding metric for policy, even though no economist has ever been able to explain exactly how inflation works, let alone predict when it will increase or decrease. On her (excellent) Substack, Claudia Sahm praises Rudd’s paper as “a call to action” and “a plea for us to really understand inflation.”

“We are living with the highest inflation in decades—though the monthly pace is stepping down and the pandemic, which is the source of many supply chain bottlenecks and labor shortages, is slowly getting under control,” Sahm concludes. “And at the same time, the Fed is using a new, untested inflation strategy. The world is tough, and forecasting near impossible. Now is not the time to be using broken tools.”

Spicy! And what does any of this mean for the purposes of ordinary Americans? At this point, not all that much. But it’s a real Emperor’s New Clothes moment for the economics profession in general, and the Federal Reserve in particular. At a time when the use of the word “unprecedented” has reached unprecedented new heights, it’s important for our leaders to remember that they don’t know everything, and to stop pretending that they can predict what’s going to happen next.

In short: It’s now obvious that economists at the Fed and elsewhere can’t predict the future with any sort of accuracy, so instead they should work as hard as they can to solve the real problems that they see in front of them—rampant income inequality, a housing crisis that will only get worse as local eviction bans continue to expire, and other pandemic-caused economic troubles—rather than prepare for inflation panics that very well may never materialize.

Be kind. Be brave. Mask up. Get vaccinated.

Zach