Which side are you on?

Which side are you on?

The Pitch: Economic Update for August 4th, 2022

Friends,

The economics world has publicly and aggressively fractured over the Federal Reserve’s push to raise interest rates. It’s rare that arguments between economists happen in broad daylight like this, but we do not live in ordinary times.

The crux of the matter is that the Federal Reserve is cranking up interest rates in an effort to cool down the economy and lower inflationary high prices. Larry Summers, the former Clinton and Obama Administration economist, has gone on a tour to support the Fed’s decision—but he also claims that raising interest rates will have to go much higher and will need to result in massive unemployment to get inflation under control. You read that right: he argues the only way to handle high inflation is make the economy worse and put millions and millions of people out of work.

The Fed responded to Summers’s claims in a report arguing that it’s possible to cool the economy and lower inflation while keeping the number of unemployed Americans relatively low, compared to historical levels.

“The fight is playing out in wonky academic papers, but the real world stakes for workers are high,” explain Neil Irwin and Courtenay Brown at Axios. “At odds is not whether unemployment rises, but by how much as the Fed tightens.”

Meanwhile, esteemed economists like Arindrajat Dube are joining the fray on a third front: They argue that raising interest rates isn’t even the correct way to combat pandemic-inspired inflation. “The instinctual response of some economists to immediately blame inflation on an over-tight labor market where nominal wage growth is driving inflation is belied by the very simple fact that...real wages are falling (except at the bottom),” Dube tweeted. Other economists on the left end of the political spectrum are joining Dube’s side, including an excellent piece in Dissent from Brian Callaci and Sandeep Vaheesan which states flatly that “tight labor markets are simply not the cause of the current surge in inflation.”

So in order to rein in inflation, one side argues that the economy needs to be cooled down by forcing millions of workers onto unemployment for years, another side argues that the economy still needs to be cooled down but that it’s possible to keep unemployment levels low compared to past recessions, and a third side argues that cooling the economy down is unnecessary.

It’s a dispute over how to organize our understanding of the economy: Do we prioritize the super-rich who can easily weather a recession, do we prioritize the ordinary American over the wealthy few, or do we quibble over how many suffering Americans are enough?

It’s historically rare for an economic dispute to split along three distinct fronts like this, and this fractured landscape could change the face of economics for the foreseeable future, much the same way that the rise of trickle-down economics realigned the field for 40 years. We’ve made clear in this newsletter that since broad-based consumer demand creates jobs in the economy, we’re on the side of the vast majority of American workers, and we favor policies that prioritize the many over the few. Which side are you on?

The Latest Economic News and Updates

Inside the Inflation Reduction Act

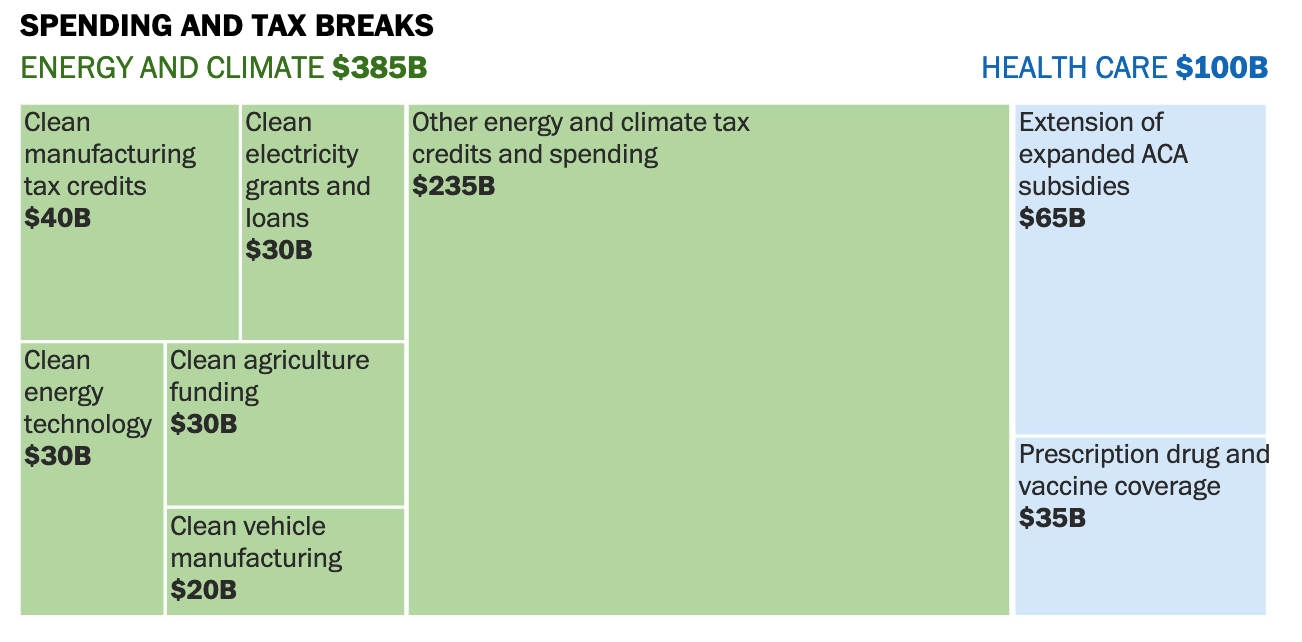

Last week, Senators Joe Manchin and Chuck Schumer announced that they’d come to an agreement on a smaller version of President Biden’s Build Back Better legislation, which they were calling the Inflation Reduction Act. In a sweeping exploration of the bill, the Washington Post notes that if it passes through the Senate, the IRA “would represent one of the most consequential pieces of economic policy in recent U.S. history,” with $385 billion in green-energy investments, $100 billion in health care investments, and over $700 billion in revenue raised through health care savings and taxes on corporations and the super-rich.

Moody’s team of economists have determined that the bill would make a small and immediate dent in inflation by taxing corporations, and it would help keep inflation down in a more meaningful way over the next decade by keeping health costs in check and lowering prescription prices. The Roosevelt Institute argues that Moody’s is underestimating the impact that IRA will have on inflation for a number of reasons including the fact that empowering the IRS to go after tax cheats will pull in more revenue than projected and the fact that healthcare is a huge pressure on inflationary prices.

Alan Rappeport and Emily Flitter at the New York Times explain that IRA’s proposed shrinking of the carried interest loophole, which is estimated to raise $14 billion in revenue over a decade, is a big deal that has been discussed in politics for years. Carried interest is one way that Wall Street elites pay less in taxes than the rest of us. It’s “the percentage of an investment’s gains that a private equity partner or hedge fund manager takes as compensation,” they write. “Under existing law, that money is taxed at a capital gains rate of 20 percent for top earners. That’s about half the rate of the top individual income tax bracket, which is 37 percent.”

Yesterday, though, the news broke that Arizona Senator Kyrsten Sinema opposes closing the carried interest loophole, supposedly because it “could undermine economic competitiveness,” though the real reason might have more to do with the fact that private equity firms lobby extensively with Sinema’s office.

The fate of IRA is up in the air—by the time you read this, it may have passed, or it may have been shot down, or it may be on pause. But it’s still important to note that it represents a significant change in progressive economic thinking—an investment in America that rejects the trickle-down fallacy that tax cuts for the rich are what creates jobs and economic growth. No matter how IRA works out in the end, it’s another sign that most Democrats are developing an understanding of the economy that doesn’t rely on trickle-down orthodoxy.

Tax migration isn’t a real thing

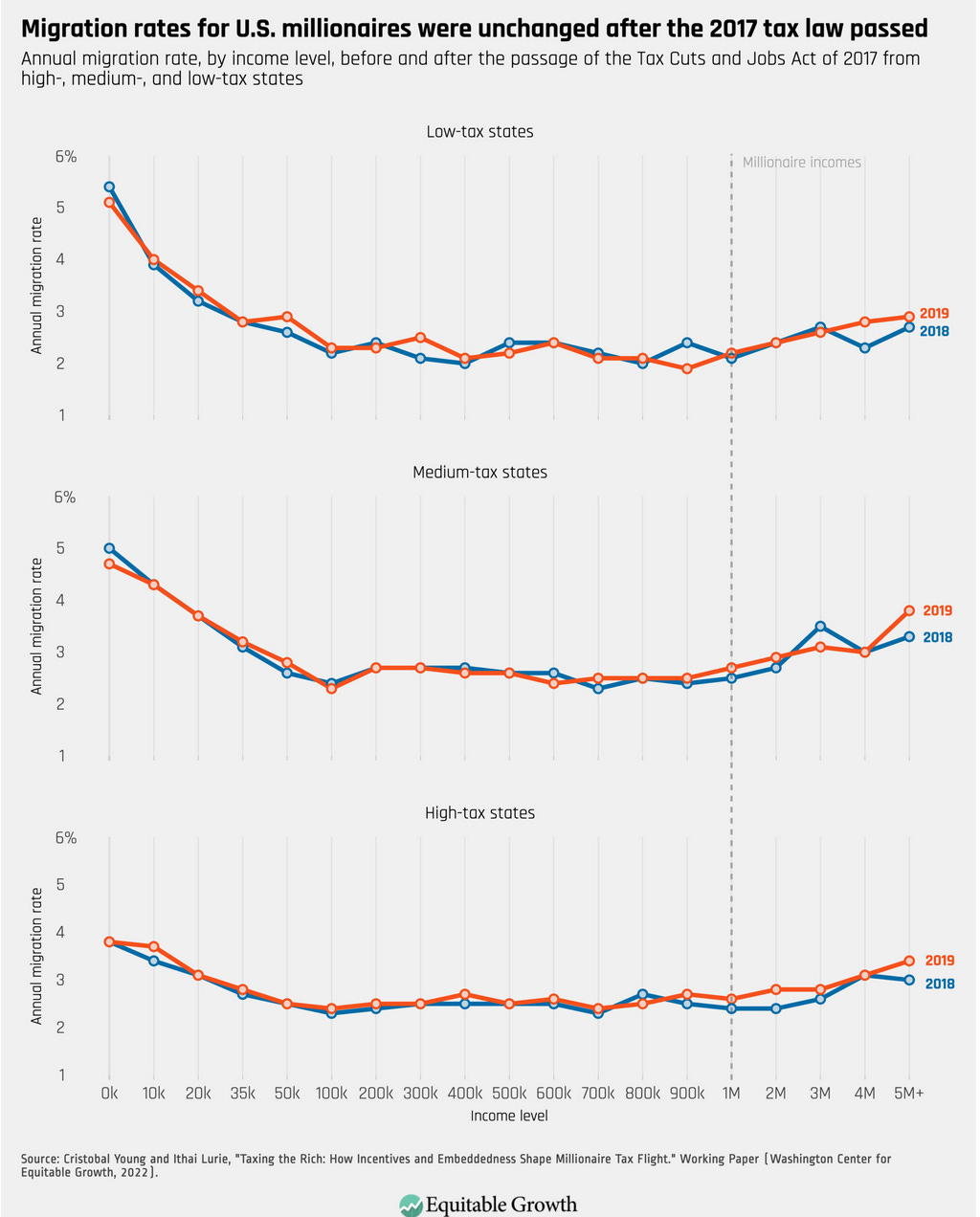

Speaking of trickle-down orthodoxy, one of the big threats that conservatives love to pull out when anyone considers raising taxes on the rich at a state or city level is that doing so will simply cause wealthy people to move away. We saw threats like this in Washington state last year when the legislature finally passed the state’s first capital gains tax, and during the pandemic a few loud billionaires made a point of saying they were moving to states with no income tax, inspiring a panic in blue states like New York and California.

But a new study from the Washington Center on Equitable Growth studying the migration patterns of millionaires finds that tax flight isn’t really a thing, unless the millionaires in question were already going to move: “taxes do not affect the decision to move, but, conditional on moving, they do influence the choice of destination—making low-tax states incrementally more attractive,” the authors write. So does this mean states should cut taxes in the hopes that a small number of millionaires would want to move there? In short, no: “if states cut taxes in an effort to attract millionaires, the revenue losses would far exceed the gains,” they conclude.

So are we in a recession or not?

We talked a lot last week about whether or not we’re in a recession, and why the media’s repetition of recession fears might be likely to cause a recession. This week, the Dallas Federal Reserve issued a report that argues fairly conclusively that we are not in a recession despite negative GDP growth. Specifically, “most indicators—particularly those measuring labor markets—provide strong evidence that the U.S. economy did not fall into a recession in the first quarter.”

The Fed’s report is full of charts comparing current economic conditions with those of past recessions, and our current economy (illustrated below with red lines) bears almost no resemblance to even the smallest recession in recorded history:

The New York Times shows that consumer spending has slowed to “a crawl,” which is obviously bad news, but spending has also largely transferred from goods to services, which “might be a welcome trend.” If consumer spending is switching over to services rather than disappearing entirely, that’s a sign that consumers are still on somewhat solid footing. (And remember that spending on services plummeted during the pandemic for obvious reasons. Services spending only just reached pre-pandemic levels in May of this year.)

There are still some troubling signs. Manufacturing numbers are slowing down slightly (though inputs at factories—basically, the cost of goods for manufacturers—have reached two-year lows, which Reuters says could mean that “inflation has probably peaked.”) Credit card debt has reached 20-year highs as consumers continue to absorb higher prices, with Americans underneath two trillion dollars more credit card debt than they were before the pandemic. And the number of job openings in America fell a bit in June, though demand for workers is still near record highs.

As I pointed out in the introduction, there’s a contentious debate unfolding in the economics sphere right now about what we should do in response to these weird numbers and their bizarre array of economic signals warning that we are or are not at risk of a recession. Josh Bivens at the Economic Policy Institute warns that the Fed is getting dangerously close to pushing us into an unnecessary recession at a point when inflation looks to be calmer than at any point since early 2021.

And some of the best writing I’ve seen on the risks of the Fed’s action comes from Zachary Carter’s Substack, with a clear-eyed look at FDR’s response to the Great Depression and what the human costs of the Fed’s action will be:

Anyone who calls double-digit unemployment a solution to anything does not belong in politics. But the reasoning in play here should simply horrify people who believe in democracy. The most important cost-of-living issue for families this year is housing – in many cities, rent has exploded. Ask yourself: if the goal is lower rent, should we a) build more houses, or b) indiscriminately fire a large number of people from their jobs? The latter is the serious contention of this newly revived austerity brigade.

Costs are up, and we all pay the price

The Washington Post published an incredible visualization showing the different rising prices that have driven inflation during every month of the last couple of years. In early 2021, used cars and travel and restaurants led the price increases, while housing and grocery prices have been higher in early 2022. Perhaps most unsurprisingly, energy prices have been consistently high since Russia’s invasion of Ukraine. Gwinn Guilford at the Wall Street Journal warns that volatility in the energy market could keep energy prices high for the foreseeable future, and inflation up for years.

Of course, the kicker to those high prices we’re all paying for energy is that Big Oil profits continue to skyrocket, with Exxon and Chevron reporting record profits in the second quarter of 2022. “Exxon took home $17.6 billion, while Chevron made $11.4 billion. That translates to $2,245.62 a second for Exxon and $1,462.11 a second for Chevron. Nice work if you can get it,” writes Dan Crawford at Cost of Greed. It’s not just Exxon and Chevron, either: BP reported that their profits tripled in the second quarter of this year.

But while Big Oil executives revel in their record profit margins, Americans are increasingly turning to dollar stores for their grocery shopping—a sure sign that many of us are being priced out of grocery stores. “Average spending on groceries at discount chains shot up 71% between October and June. Spending at big-name stores decreased by 5%,” writes Markie Martin at News Nation.

And of course, housing prices continue to be out of reach for too many Americans. If you’re interested in reading an interesting policy proposal to address skyrocketing housing costs, I’d recommend Ramenda Cyrus’s piece about social housing in the American Prospect, which she argues is a step toward making housing a right for everyone:

For example, a municipality might have an apartment building in which a third of the units were deeply subsidized for low-income people, a third provided at cost for the middle class, and a third at the market rate open to anyone. Every segment of the housing market, from top to bottom, would get more supply simultaneously.

Uneven wages make for a choppy job market

Paul Krugman in the New York Times explores the relationship between wages and commodity prices. Over the span of decades, you can watch oil prices go up and down almost erratically, but wages in America stay steady with a very modest incline over time. Krugman concludes that wages don’t decline and spike erratically because, well, workers are people and not barrels of oil. If employers tried to drive wages down to meet market conditions, people would revolt. Krugman makes the case that wage gains could hold inflation aloft for a while longer simply because they’re inelastic.

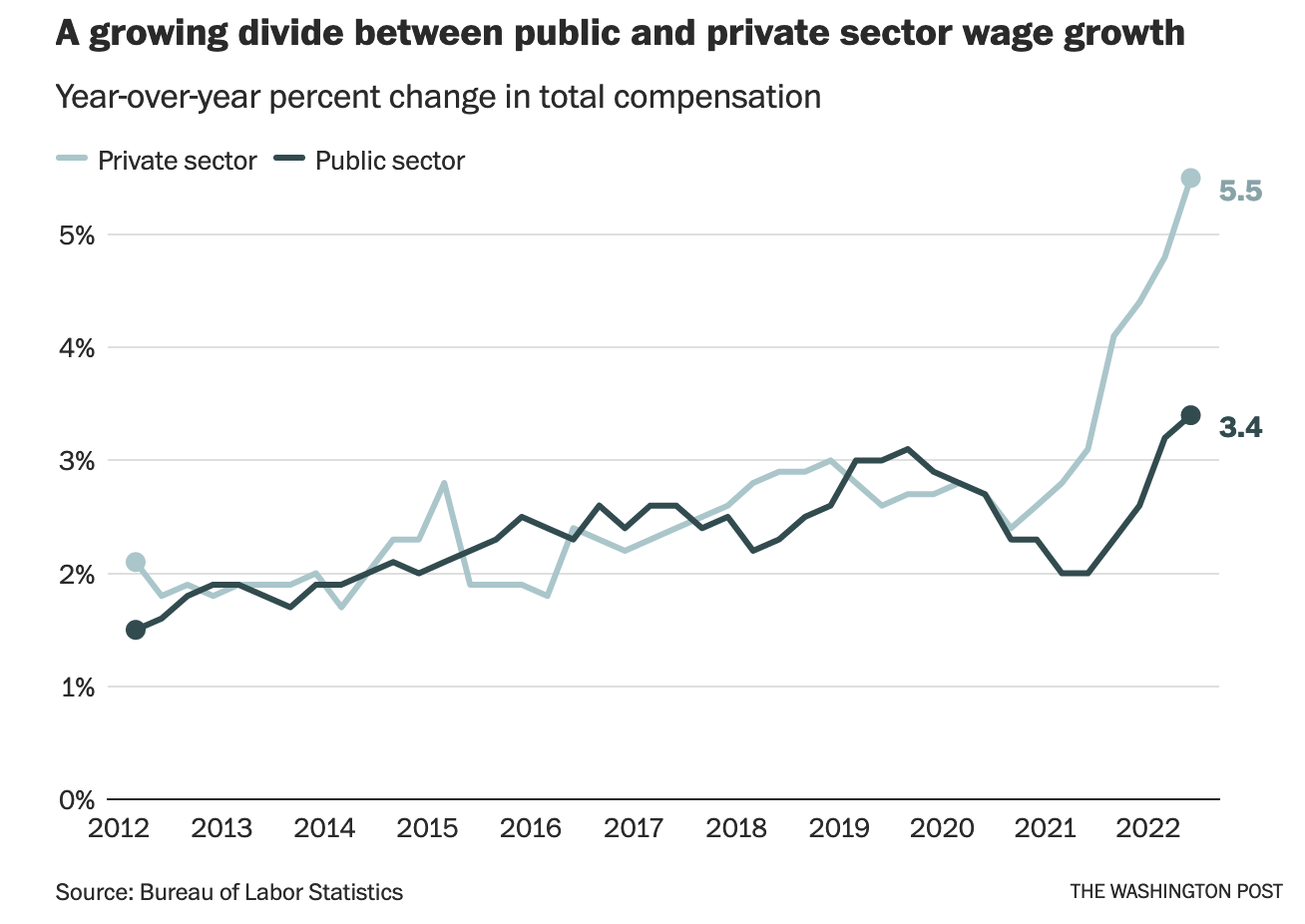

But the truth is that wage gains aren’t shared equally across all workers. For instance, government wages have lagged way behind private-sector wages throughout the last couple of years, and so public sector worker pay is way down when you take inflation into account.

Axios put an interesting spin on job numbers this morning with the theory that businesses are “hoarding workers” by not committing to layoffs that would have happened by now in the past. Because the job market has been so strong for workers, “some employers have said they are hesitant to reduce headcount, even as growth deteriorates.” A survey of corporate earning calls found that 18 percent of publicly traded companies say they’re continuing to hire, while just three percent admit that layoffs are likely.

Those CEOs are right to be concerned about hiring issues: There is still more than one job opening for every worker looking for a job, and so workers have more power than at any time in recent memory. That’s probably part of the reason why the first American Trader Joe’s voted to unionize last week in Massachusetts. For many years, Trader Joe’s was considered an excellent employer, but since 2010, the company has sliced away at its health insurance and retirement plans, leaving workers with little recourse but to take collective action.

Krugman was right: You’ll never see barrels of oil form a picket line, but push people too far, and they’ll start to demand a fair shake from their bosses. For as long as the labor market stays pointed in the direction of workers, we’ll continue to see this kind of organizing.

Real-Time Economic Analysis

Civic Ventures provides regular commentary on our content channels, including analysis of the trickle-down policies that have dramatically expanded inequality over the last 40 years, and explanations of policies that will build a stronger and more inclusive economy. Every week I provide a roundup of some of our work here, but you can also subscribe to our podcast, Pitchfork Economics; sign up for the email list of our political action allies at Civic Action; subscribe to our Medium publication, Civic Skunk Works; and follow us on Twitter and Facebook.

On Civic Action Live this week, we’ll be examining Friday morning’s jobs numbers and what they mean for recession fears, we’ll explore the economic policies in the Inflation Reduction Act, and we’ll get to the bottom of why economists are arguing so ferociously over the Fed’s decision to raise interest rates. Join us on Friday at 10:30 am PST.

Professor Mariana Mazzucato joins this week’s episode of the Pitchfork Economics podcast to discuss the thesis of her latest book: The idea that government needs to direct policy more often into “moonshot”-style aspirational programs (like solving the climate crisis) in order to focus America’s economic might toward goals that benefit everyone.

And in his Business Insider column, Paul explains that CEO pay has been skyrocketing at the same time that the minimum wage has hit historic lows in value. Those two facts aren’t unrelated.

Closing Thoughts

The American Economic Liberties Project recently published an important policy brief on a growing problem at the intersection of local government, unchecked corporate power, and worker rights: “All across the country, mayors, city councilors, governors and officials at economic development boards – which are public or quasi-public agencies that negotiate economic development deals – have signed non-disclosure agreements when doling out corporate subsidies,” the authors write.

Giant corporations like Google, Amazon, and General Motors basically negotiate with local leaders for giant tax breaks, subsidies, and other giveaways, and then tie up those sweetheart deals in a thicket of NDAs and other legal barriers so that the public can’t learn about them. In recent years, the power balance has tipped almost entirely in the favor of corporations.

Some leaders have even negotiated tens of millions of dollars in giveaways with lawyers before they’re even allowed to learn which company they’re negotiating with. That’s not hyperbole: One Oklahoma state Democrat publicly wrestled with the anonymity of these deals: “How am I supposed to go back to my constituents and say, ‘I gave away three-quarters of a billion dollars to a company that I don’t even know their name?’ Is that responsible?”

Because of the secretive nature of these NDAs, it’s impossible to know exactly how much money has been given away to corporations in exchange for corporate investments in the past decade or so, but the examples we do have of secret corporate subsidies total in the billions of dollars. That’s revenue never collected, regulations lifted, and other funds given back to corporations before they even dig up one shovel’s worth of dirt on a new data center, or hire one local for a new manufacturing plant.

The good news is that it’s relatively simple to outlaw this kind of secret negotiation. “The goal of this legislation is not to ensure that every aspect of the negotiations happen in public,” the authors write, “but that vital information – the who, when, why, and how much of corporate subsidies – happens in public, and that there is opportunity for public organizing and input before a deal is closed.”

And these policies are deeply popular. Polling from this summer found that “71 percent of respondents said that they were more likely to support a candidate who favors banning backroom subsidy deals negotiated without public input.”

While businesses have to keep secrets in order to stay competitive, transparency is an important ingredient in a functioning democracy. When business and government overlaps, the people need to be able to understand the broad contours of what their leaders are negotiating away. Otherwise, the possibilities for corruption and corporate malfeasance are too great. So far as popular public policy goes, this is a no-brainer for local candidates to embrace.

Be kind. Be brave. Get vaccinated—and don’t forget your booster.

Zach