Who Killed the Instant Pot?

The Pitch: Economic Update for June 22, 2023

Friends,

You may have read that Instant Brands, the company behind the Instant Pot line of pressure-cooker devices and the Pyrex brand of high-quality glass kitchenware, filed for bankruptcy last week. Considering the fact that Pyrex has been popular in kitchens for generations, and Instant Pots were the must-have holiday gift several years ago, this news might strike you as bizarre. How can a business that manufactures two of the most successful cooking brands in the world fail so badly that it winds up going bankrupt?

Most news stories about the bankruptcy blamed the pandemic for Instant Pot’s precipitous fall: With everybody working from home, the argument went, there was no need for home chefs to rely on “set it and forget it” cooking methods like the Instant Pot. And while the pandemic definitely changed the way we use our kitchens, that excuse simply doesn’t explain the full scope of the decline and fall of Instant Brands.

No, the real villain in this story is a familiar one: Private equity. “Instant Brands is majority owned by Cornell Capital, a New York-based private-equity firm that engineered the 2019 merger after initially purchasing locally based World Kitchen, the Pyrex and CorningWare company, in 2017,” writes Steve Daniels at Chicago Business.

Once Cornell Capital bought in, they immediately started sucking all the profits out of the businesses and away to wealthy investors. And when Americans bought lots of Instant Brands products when they took to their kitchens during lockdowns in the early days of the pandemic, Daniels continues, Cornell decided to take a big loan against all that new revenue and pay it out directly to shareholders:

In April 2021, in the midst of that sunny period, Instant Brands took on a $450 million term loan, according to the filing. That debt refinanced $294 million in existing debt, including $100 million tied to the 2019 acquisition, and helped support a $245 million dividend to the shareholders, according to a Moody’s rating of the loan in May 2021.

Essentially none of the debt, then, supported investment in the business.

Classical economists teach that when businesses profit from innovation or good timing or some conflation of the two, those businesses then invest the money back into the product, sharing profits with workers and innovating new ways to keep profits flowing in. But private equity airlifts the money up and away from profitable companies and toward the wealthy shareholder class, and then saddles the company with an enormous amount of insurmountable debt. Finally, once all available short-term value has been sucked out of the company, private equity firms sell off its remaining husk for scraps.

It’s unlikely that Instant Pots and Pyrex cookware will disappear from American kitchens in the long term. Some other corporation will likely scoop up the remains of the two valuable brands for pennies on the dollar. But nobody can predict if the next-generation Instant Pots and Pyrex will maintain the quality that made both brands so beloved, or if they’ll just be zombie brands, resurrected in a cheap and shoddy manner to take advantage of the familiarity of the name.

We’ve already seen this dance play out with brands like Toys R Us, Sears, and Payless Shoes, and unless we pass some policies to combat this kind of predatory behavior, we’ll see it happen again. Elizabeth Warren has already written and cosponsored legislation that would require private equity to limit the profits they can quickly suction out of a firm, and would tie private equity companies to the failure of the companies that they intentionally destroy.

As it is, private equity firms manage to avoid risk and accountability by driving companies into the ground and laying off workers in exchange for a quick payday. This kind of extractive, destructive behavior harms many Americans in exchange for huge paydays landing in the pockets of a wealthy few, and it is exactly the kind of behavior that regulations exist to counter. This will keep happening until our leaders make it stop.

The Latest Economic News and Updates

The Inflation Distortion Field Is In Full Effect

Paul Krugman looks into why every positive inflation report is greeted with muddled headlines, and he talks about how the way we measure inflation is confusing and overcomplicated. For instance, Krugman’s chart showing what inflation would look like without housing and used cars (which tend to be lagging indicators that hold inflation numbers high for months after other numbers decline), and food and energy prices (which can scramble overall inflation numbers with their volatility) included shows a marked and very clear decline:

And our fight against rising prices is outpacing many other nations—for instance, the United Kingdom’s inflation rate is standing at 8.7%. But of course, Americans don’t make any nuanced distinctions about foreign and domestic inflation numbers when they buy groceries, or shop for a used car. Prices are prices. If the price of eggs are plummeting but the price of bread is rising, that bill at the end of the shopping trip is still going to be higher than normal.

Less than a week after Krugman wrote his piece criticizing the media’s muddled takes on inflation, his own newspaper, the New York Times, published a piece by Jeanna Smialek that expertly plays the both-sides game Krugman laments:

The economic picture, in short, is playing out on something of a split screen. While the steepest price increases appear to be over for consumers — a relief for many, and a development that President Biden and his advisers have celebrated — Fed policymakers and many outside economists see continued reasons for concern. Between the subtle signs that inflation could stick around and the surprising resilience of the American economy, they believe that central bankers might need to do more to cool growth and rein in demand to prevent unusually elevated price increases from becoming permanent.

Smialek is a smart economics reporter we have praised many times in this newsletter, but in this instance, I do have to note that in the above paragraph, she has framed “the surprising resilience of the American economy” as a negative development in the fight against inflation. This is the kind of nonsense that you get when you talk with economists who only measure our nation’s economic health by how it affects the wealthiest few at the top of the economy.

Smialek isn’t the only reporter repeating this ridiculous claim: Nick Timiraos wrote yesterday in the Wall Street Journal that Fed officials are trying to balance the risk of an economic slowdown “against the risk that the economy proves more resilient than expected and inflation stays too high, requiring them to increase rates higher than otherwise.”

Let’s say this as plainly as possible: A resilient economy is a good thing. If the economy weren’t resilient, millions more people would now be out of work. And lower prices wouldn’t matter if those millions of unemployed people can’t afford to buy any groceries for their families. The idea that resilience is a negative quality is peak neoliberalism-ate-my-brain in action.

Even the Wall Street Journal’s James Mackintosh seems to think all the obsession over the Fed’s actions has gone too far: “There is plenty of evidence that the economy is getting better, rather than worse. The Atlanta Fed’s GDPNow estimate of the current quarter drawn from data released so far puts growth close to 2%, way higher than the slight fall economists predicted at the start of April,” he writes. “Consumer sentiment is up, according to preliminary figures from the University of Michigan, while inflation expectations are down. Even the highly interest rate sensitive home-construction market is showing signs of life.”

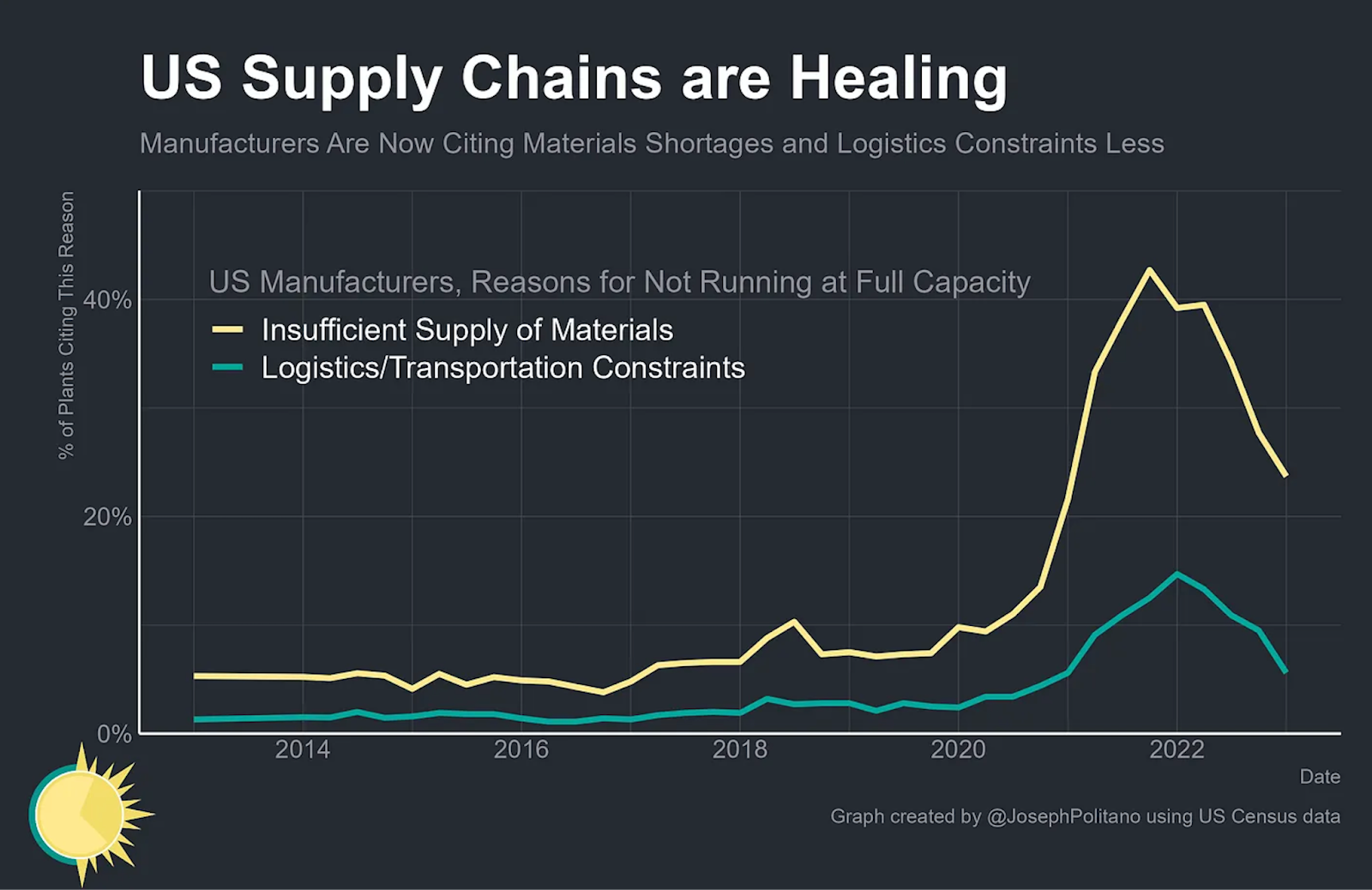

Finally, in news so good that even economists can’t deny it, the supply chain issues that caused the price increases we paid in 2021 are finally becoming a distant memory. Joseph Politano at Apricitas Economics reports that “the worst of the supply-chain crisis is definitely behind us. Manufacturing output in key industries has recovered to pre-pandemic levels, materials shortages are abating, and international trade networks are normalizing.”

For the New York Times, Patricia Cohen writes about why our perception of globalization has changed so dramatically since 2018, when the head of the IMF declared that the global economy was “in a very sweet spot.”

Cohen writes that in 2018, “The favored economic road map [of globalization] helped produce fabulous wealth, lift hundreds of millions of people out of poverty and spur wondrous technological advances.”Cohen acknowledges immediately after that “there were stunning failures as well. Globalization hastened climate change and deepened inequalities.” When the pandemic arrived, and when Russia invaded Ukraine, those deepened inequalities became even more evident to everyone. And at the same time, nations around the world experienced dramatic climate events like flooding, droughts, and raging fires.

It’s interesting to go back to the supposed glory days of 2018 and see how the New York Times’s Neil Irwin characterized the state of globalization: As a net positive for the world, but one under threat from anti-globalization forces, which he characterizes as “coming at exactly the wrong time — too late to do much to save the working-class jobs that were lost, but early enough to risk damaging the ability of rich nations to sell advanced goods and services to the rapidly expanding global middle class.”

So across the span of five years, the Times has evolved from framing globalization as precarious and under assault to…framing globalization as precarious and under assault.

The 2018 story does at least correctly identify widespread consumer spending as the true driver of economic growth and prosperity. But it fails to recognize that the people who most profited from globalization were the wealthy few—the corporations, CEOs, and people wealthy enough to profit from the exploitation of workers.

The unmistakable lesson of these two stories is that you can’t take shortcuts when your goal is to build a strong economy. Globalization was sold to the masses as a way to build a global economy in which consumers around the world share in unprecedented prosperity. But in the short term, corporations and the wealthy few raked in unprecedented profits by exploiting cheap labor in low-wage nations—and then those same corporations were shocked to find that there aren’t enough consumers participating in the economy to encourage the kind of economic growth that we saw at the beginning of the 21st century.

This divided economy has increased income inequality here in the United States, and it’s likely to increase global inequality unless we take action to end it by building a global trade strategy that prioritizes ordinary people, not corporations and the wealthy.

Are Democrats and Republicans Realigning on Economic Issues?

David Leonhardt in his newsletter, writes that “A rising generation of Republican politicians is more skeptical of the free market and more comfortable using government power to regulate the economy than the party has traditionally been.”

There’s certainly something to the idea: Since Donald Trump started talking in the language of economic populism, Republican politicians have started to reject some of the trickle-down tenets that have dominated their party since the Reagan administration. Republicans are now less likely to defend big banks and their CEOs, and as we saw during the debt ceiling debacle, Republicans rejected the idea of Medicare or Social Security cuts, which have been part of their platform for decades.

But it’s complicated. There are plenty of Republicans who haven’t yet thrown off the trickle-down yoke. Republican Congressmembers are still trying to sneak cuts to Social Security into bills like a proposed paid family medical leave act. And while Trump talked a lot about returning wealth and prosperity to working Americans, his one signature accomplishment was a huge tax cut for wealthy people and corporations. So it’s exceptionally premature to declare the GOP thirst for trickle-down as dead and buried.

To see the difference between these two economic philosophies in action, consider David Dayen’s overview of dueling banking regulation reforms being discussed in the Senate to respond to the bank failures from earlier this year. One measure was promoted by Senator Elizabeth Warren, and the other was a bipartisan deal worked out between Senators Sherrod Brown and Tim Scott, who is currently running for president in the Republican primary.

“First and foremost, the Warren bill would require the FDIC to claw back all or part of the compensation [bank executives] received over a three-year period before a bank failure; Brown-Scott makes it discretionary,” Dayen writes. “Warren initially let regulators claw back five years’ worth of executive compensation; to get other Republicans on board, she dropped it to three. Brown-Scott reduces that further to two.”

So let’s be clear: Republicans have a long way to go. Their policies still largely favor the wealthy over working Americans, and we should always measure politicians by the policies they actually pass, not the ideals they claim to embrace in their speeches.

Measuring the Social Safety Net

The full paper is very wonky, but I do want to make sure you see this paper in The Review of Economic Studies, which studies the long-term effects of the social safety net in children. The part you should take to heart is the bolded selection from the abstract below:

We find that children with access to greater economic resources before age five have better outcomes as adults. The treatment-on-the-treated effects show a 6 percent of a standard deviation improvement in human capital, 3 percent of a standard deviation increase in economic self-sufficiency, 8 percent of a standard deviation increase in the quality of neighborhood of residence, a 1.1-year increase in life expectancy, and a 0.5 percentage-point decrease in likelihood of being incarcerated. These estimates suggest that Food Stamps’ transfer of resources to families is a highly cost-effective investment in young children, yielding a marginal value of public funds of approximately 62.

This study adds to a huge body of research showing that investments in the quality of life of children result in happier, healthier, more economically sound adults. In other words, if we invest a little bit of money in children today, we’ll spend less on them as adults later. Remember this study the next time you see a politician suggest saving a few bucks by making it harder for families to access food stamps and housing benefits.

Fighting for the Future of Work in America

Employers are still adding workers at a significant clip, but the Labor Department says those workers are putting in slightly fewer hours on the job, according to the Wall Street Journal.

Nobody can specifically identify why this is happening. Employees working fewer hours is usually a sign of an oncoming recession, but employers don’t add workers to the payroll when recessions seem imminent. The most likely reason suggested in the article is this one: “Businesses are finally able to hire for long-unfilled positions, allowing overworked staff to return to more normal hours. Finally, workers are opting to work less, possibly because of a shift in work-life priorities.” For instance, “In May, the average factory worker had 3.6 overtime hours [per month], down from 4.1 a year earlier.”

The labor market remains strong enough that workers continue to demand more pay and better working conditions from their employers. For instance, UPS union workers recently authorized a possible nationwide strike for later this year. If they do strike, it will be “the largest of any U.S. industry since the 1950s,” according to the Washington Post.

While UPS workers were able to successfully demand air conditioning in their delivery trucks during recent negotiations, they want more from their employer including “higher pay, the creation of more full-time jobs and the elimination of UPS’s reliance on a lower-paid class of delivery driver.”

Other companies continue to push back against workers who have successfully moved to unionize. The Washington Post follows a Starbucks barista named Lexi Rizzo who was fired after years of employment for being one minute late to a shift. The fact that Rizzo also helped to unionize her Starbucks store explains why management might have been eager to get rid of her...

“In the last year, judges have ruled that Starbucks violated U.S. labor laws more than 130 times across six states, among the most of any private employer nationwide,” writes Greg Jaffe. “The rulings found that Starbucks retaliated against union supporters by surveilling them at work, firing them and promising them improved pay and benefits if they rejected the organizing campaign.”

Meanwhile, Senator Bernie Sanders launched an investigation into Amazon’s labor practices, alleging that the company’s warehouses are unsafe for workers, and that Amazon has participated in illegal anti-union practices.

While the flood of headlines about workers voting for unionization last year has slowed to a trickle, there are still enough workers calling for better pay and benefits every day to keep workers’ rights perpetually at the top of the news cycle. As long as the economy stays resilient, we can expect workers to continue to loudly advocate for themselves. And yes—with all due respect to the New York Times and Wall Street Journal—that’s a very good thing for the economy.

Real-Time Economic Analysis

Civic Ventures provides regular commentary on our content channels, including analysis of the trickle-down policies that have dramatically expanded inequality over the last 40 years, and explanations of policies that will build a stronger and more inclusive economy. Every week I provide a roundup of some of our work here, but you can also subscribe to our podcast, Pitchfork Economics; sign up for the email list of our political action allies at Civic Action; subscribe to our Medium publication, Civic Skunk Works; and follow us on Twitter and Facebook.

Is it possible to improve the planet for all humanity while helping the planet survive climate change? In the latest episode of Pitchfork Economics, economist Andrew Fanning joins Goldy and Nick to talk about Doughnut Economics, a burgeoning movement that aspires to rewrite economics to prioritize the basic needs of all humans and balance that prosperity with the ecological well-being of the planet Earth.

Closing Thoughts

In all the wall-to-wall news coverage of indictments, you may have missed that President Biden gave the first real speech of his 2024 presidential campaign at a union rally last week. I wanted to flag the speech, though, because it offers a window into the Biden/Harris reelection campaign strategy.

Happily, the speech was laser-focused on economic issues. Biden began by praising the thousand middle-class union workers in the room for powering the American economy: “If the investment bankers in this country went on strike tomorrow, no one would much notice,” Biden began. “But if this room didn’t show up for work tomorrow or Monday, the whole country would come to a grinding halt.”

Biden then made a case for his economic accomplishments—inflation down by more than half what it was last year, 13 million new jobs created in the first half of his term, unemployment near a 50-year low with record lows for Black and Hispanic unemployment. And he pointed out the kind of jobs he’s been creating: “We’ve created 800,000 manufacturing jobs. And as you heard me say before: Where in God’s name is it written that America can’t lead the world again in manufacturing?”

The speech then made the important rhetorical turn of pointing out the flaws in the opposing economic theory of trickle-down economics: “Forty years of handing out excessive tax cuts to the wealthy and big corporations had been a bust. Democrats as well as Republicans did it,” he said. That wealth didn’t trickle down. “All it had done was hollow out the middle class; blow up the deficit; ship jobs overseas; strip the dignity and pride and hope out of a community, one after another, all across America as the factories shut down,” Biden said.

“We decided to replace this theory with what the press has now called ‘Bidenomics.’” he said, adding that “it’s working.”

Biden then explained the idea behind his economic decisions. “Let me tell you what it’s about. It’s about building an economy — literally, not figuratively — from the bottom up and the middle out, not the top down. Because when the middle class does well, everybody does well. The poor have a way up, and the wealthy do just fine.”

The president has said all of this in the past, and every campaign speech needs to look forward—to propose some new policies that build on the economic record. Biden said that one policy he wasn’t able to implement during his first two years in office “was dealing with the tax code.”

“Nobody thinks the tax code is fair,” he continued. “How could it be fair when 55 of the largest corporations in America paid zero in federal income tax on $40 billion in profit? We need to get rid of some of these ridiculous special-interest tax loopholes.”

Through one such tax loophole, “Big Oil made $200 billion in profit last year, and they got a $30 billion tax break on top of it.” Biden pointed out that billionaires pay eight percent in taxes, and when an audience member shouted “ What do you pay, Joe?” the president responded, “I pay a hell of a lot more than that, man. So do you. And, by the way, [billionaires] pay a lower tax rate than schoolteachers and firefighters, lower than anyone in this room.”

It was a masterful little improvised moment, capped off by Biden’s promise that “It’s time that big corporations and the very wealthy start paying their fair share. I don’t mind them being billionaires. Just pay your fair share, man.”

By all accounts, the speech went over well in the room and even swayed a few skeptics who were unsure about the prospects of a second Biden term. And this emphasis on rebalancing the tax code so that wealthy people pay as much as ordinary Americans is a compelling one—most Americans favor taxing billionaires.

This was a promising first road test of the Biden stump speech. It sticks to economic issues, and it does so the right way—by explaining how the economy really works and by drawing a sharp contrast with the opposing economic philosophy. In future outings, I’d like to see Biden propose even more policies that would get money into the pockets of American workers by raising the federal minimum wage, restoring overtime protections for millions of salaried workers, reviving the expanded child tax credit, and fighting for the establishment of paid national sick and family leave.

When he was elected, nobody would have predicted that Biden would have successfully passed three huge, transformative economic packages through Congress. The policies I listed above are popular, and Biden has a unique talent for making the case for them on both an economic level and on a personal level. As he prepares to run on a strong economic record, it’s time for him to bet big again.

Be kind. Be brave. Take good care of yourself and your loved ones.

Zach