The Fed Takes Us in the Wrong Direction

The Fed Takes Us in the Wrong Direction

The Pitch: Economic Update for June 13th, 2024

Friends,

“Employers added 272,000 jobs in May, reflecting a booming labor market that continues to fuel the economy with workers benefiting from wages that are outpacing inflation,” wrote the Washington Post’s Lauren Kaori Gurley. This number shocked and surprised experts who were predicting the job-creation numbers to slow down. (And it should be noted that this feels like the hundredth time that experts have been shocked and surprised by good jobs numbers in the past four years, which suggests that maybe their models and economic understanding don’t reflect how the economy really works.)

Not all job creation is good news—if the economy was adding mostly low-wage, low-quality jobs, workers would be losing ground. But happily, wages continue to rise. “Average hourly wage growth accelerated sharply in May, to $34.91, up 4.1 percent from the previous year,” Kaori Gurley writes. “Wages have consistently beaten inflation for nearly a year, boosting American workers’ standard of living after years of wages falling behind inflation.”

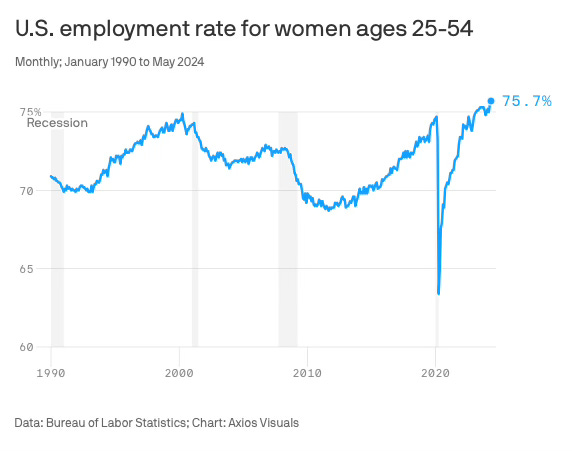

Another big revelation from last month’s jobs data is that nearly 76 percent of all women aged 25-54 have joined the workforce—a new record for female workforce participation.

You may remember that female workforce participation bottomed out during the pandemic when child care centers closed from coast to coast. As you can see in the above chart, it took years for women to get back on the job in numbers approximating pre-pandemic numbers. And this latest surge in employment is thanks, in part, to “another increase in employment in the childcare sector,” reports Axios’s Emily Peck.

It should be clear without a doubt that childcare and female workforce participation are linked—and if we want to see those numbers improve, we need to invest in childcare. (And if you’re wondering, Peck reports that “Working-age men's employment rate is hovering around pre-pandemic levels — it was 86.4% in February 2020 and 86% in May 2024.”)

We should take some space here to unpack the point I mentioned earlier, that the economic experts who have had power over the last 40 years of trickle-down economics are continually shocked and surprised by these strong jobs numbers. Remember the manufactured “nobody wants to work anymore” crisis of two years ago, or the trickle-down argument throughout the last two decades that labor force participation was on the decline, and that was somehow workers’ fault? Or the mistaken belief that millions of workers had to lose their jobs in order to get inflation under control?

All those experts who continually predict that the strong job market is about to send the American economy diving into a recession are viewing the economy through a trickle-down lens which argues that the wealthiest people and corporations are the job creators, not working Americans. So they naturally expect that the dramatic growth of paychecks and the increase of good-paying jobs will result in a collapse of the economy, because all that money is no longer rushing up to those at the tippy-top of the economy at the rate that it did during the trickle-down years.

But that’s not how the economy actually grows—as President Biden is fond of saying, prosperity grows from the middle out and the bottom up, not the top down. Workers are the most important part of the economy, and their consumer spending creates jobs. So as long as Americans are at work, and as long as their paychecks are growing, the economy is heading in the right direction. At times like these, government’s most important job is to keep investments flowing to the broad majority of Americans by combating rampant income inequality and preventing the flow of money from being hoarded at the very top of the income scale.

The Latest Economic News and Updates

Inflation Flattens Out, but the Fed Stays Put

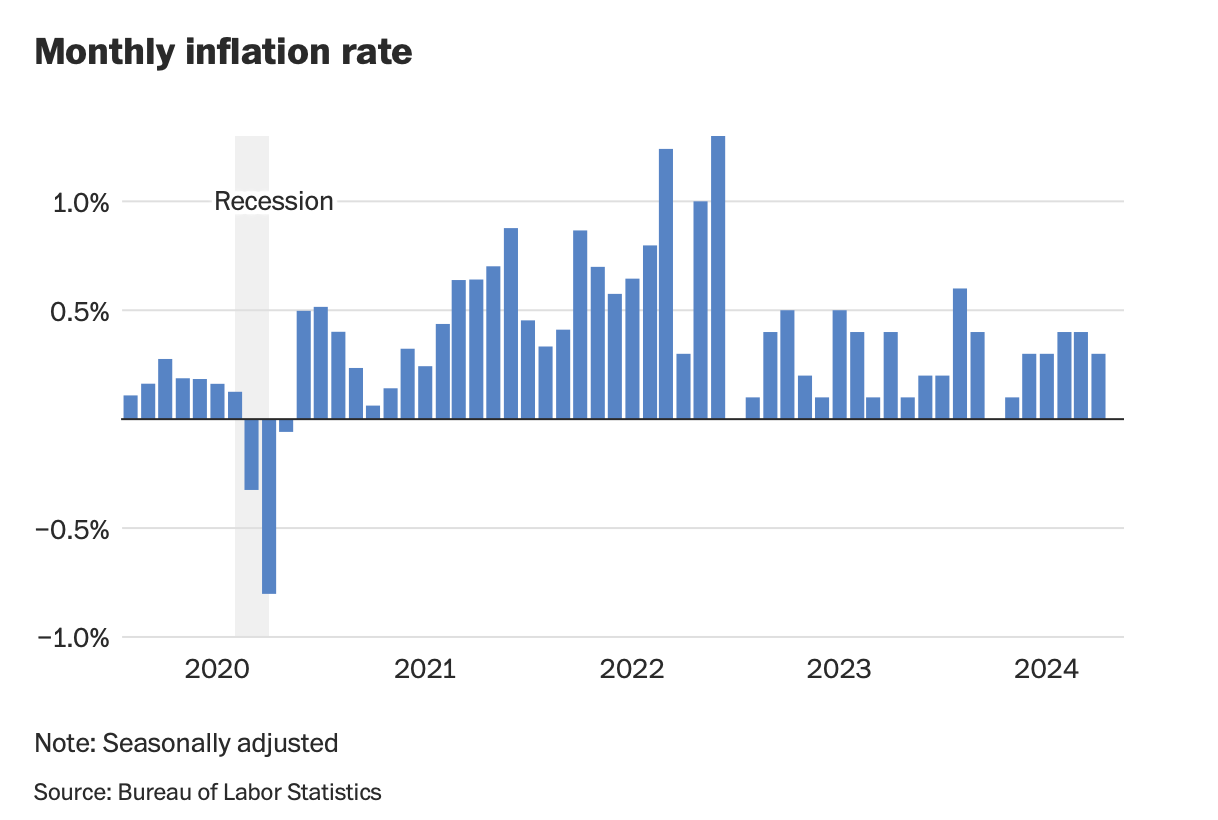

The latest report shows that inflation is headed in the right direction. “The Consumer Price Index for May was up 3.3 percent from a year earlier, lower than the 3.4 percent economists had forecast and down from the April reading,” writes Jeanna Smialek at the New York Times, adding, “if you compared May prices just to the previous month, they did not climb at all.”

The Times reports that grocery prices largely stayed flat for the past month, while transportation prices—including gas, plane tickets, and new and used cars—mostly saw big declines. “Summer vacations are cheaper and a trip to the shopping mall is getting less punishing,” Smialek writes. “It’s especially positive news when paired with recent labor market progress: Things could still change, but it is historically unusual for inflation to come down so much with such little pain.”

{kind=link}

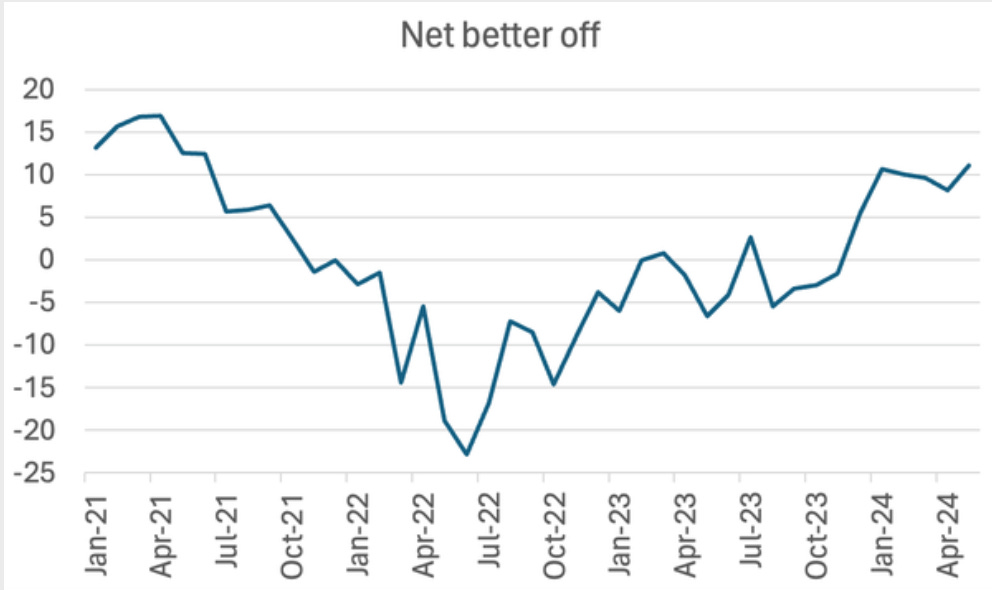

That strong job market and those leveling prices are likely responsible for improved consumer sentiment, as reported by Paul Krugman, who noted a New York Fed survey that asks consumers if they’ll be financially better off and worse off in the next year. Krugman writes, “Here’s the difference between the percentage who said better off and those who said worse off:”

“There has been a huge improvement not just since the worst of the inflation surge but even since late last year. We’re almost back to the optimism that prevailed in President Biden’s early months, before inflation took off,” Krugman writes. We have to note here that self-reported surveys are notoriously unreliable, but it does broadly correspond with some of the other economic signals we’re seeing.

Not all prices are leveling out. Medical costs increased last month, but the sector of the economy that’s really keeping inflation high has gone unchanged for over a year: Housing continues to be the biggest driver of costs for working Americans. Rachel Siegel at the Washington Post notes that “A key rent gauge carried on a streak of rising 0.4 percent over the previous month. Overall shelter costs were up 5.4 percent over the previous year.”

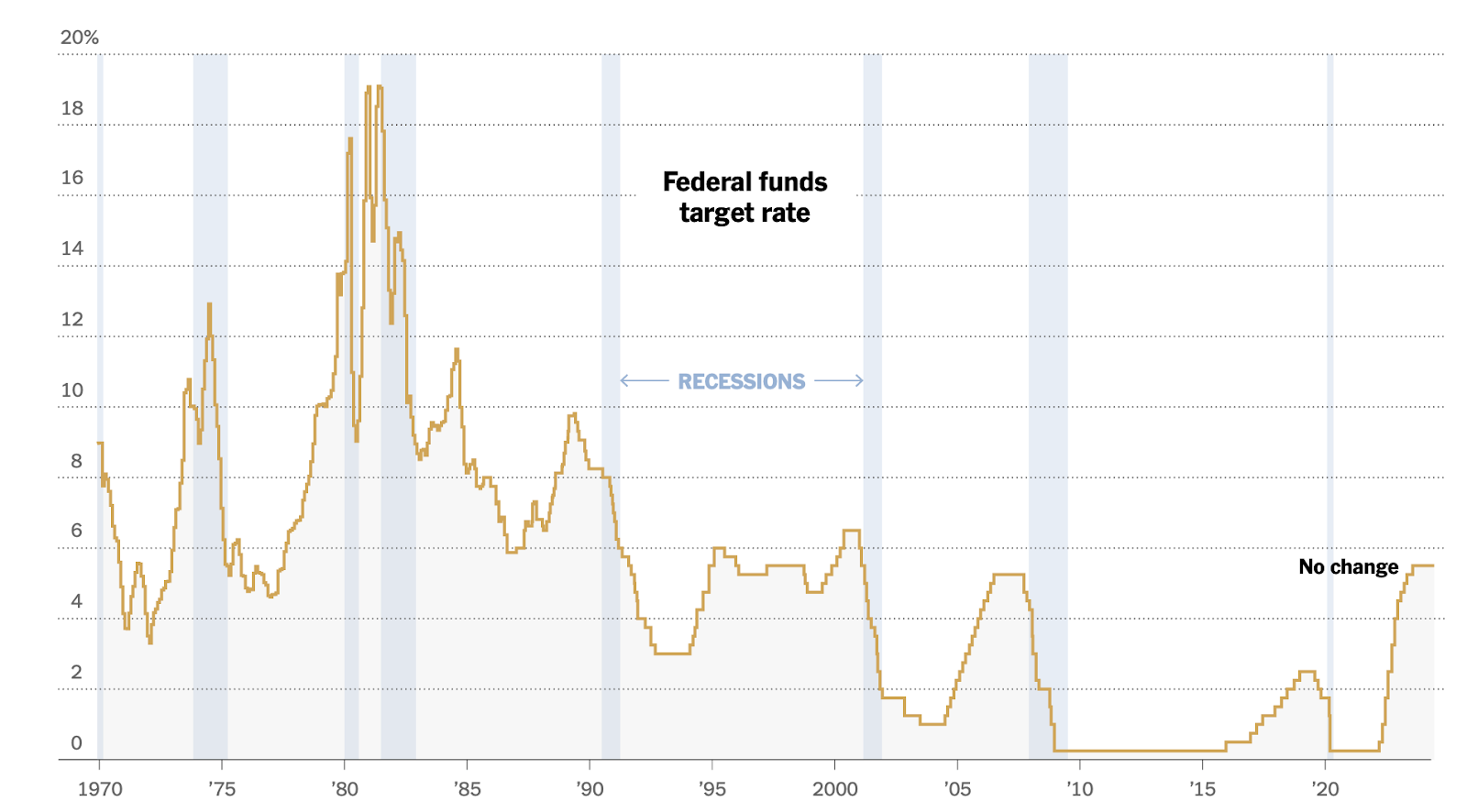

One of the biggest factors holding up housing prices for working Americans are interest rates, which the Federal Reserve has been keeping at a 20-year high as a response to high inflation. The Fed is trying to make money more expensive to borrow in an effort to cool the economy down, which supposedly would bring prices in line by curbing consumer demand. But the problem with this plan is that the prices of most consumer goods are more or less back to normal, and housing has been the most consistent driver of inflation over the last year.

So naturally you’d expect the Fed to start bringing down interest rates to lower the cost of mortgages, loans, and credit card debt, right? After all, the Fed previously announced that they would be lowering interest rates several times this year, and now that most prices except for housing have reverted to normal, lowering the interest rate would actually bring down inflation.

That would make logical sense. But that’s not what the Fed’s doing. Jeanna Smialek reported yesterday, “Federal Reserve officials left interest rates unchanged in their June decision and predicted that they will cut borrowing costs just once before the end of 2024.”

“The decision to keep rates at their highest levels in more than two decades was criticized by Democrats who have been urging the central bank to start cutting rates,” Alan Rappeport writes for the Times. “Representative Brendan F. Boyle of Pennsylvania, the top Democrat on the House Budget Committee, said after the decision that the U.S. economy is ‘being threatened by the Fed’s continuation of high interest rates’ and argued that the Fed’s actions are exacerbating a housing crisis.”

The US’s recovery from the wave of inflation that followed pandemic-era lockdowns and supply chain disruptions has been the envy of the world. In fact, the World Bank, earlier this week, announced that the global economy was in better shape than anticipated, “thanks largely to the performance of the United States,” reports David J. Lynch at the Washington Post, who adds that “The United States is the only advanced economy growing significantly faster than the bank anticipated at the start of the year.”

The Fed’s decision to keep interest rates high could push rent and housing costs even higher, and that would imperil our entire economy as more Americans fall into deep debt just to keep a roof over their heads. But perplexingly, the Fed seems to be staying put. “Despite their mostly upbeat tone, bank officials warned that central banks including the Fed are likely to move slowly to begin reversing the past two years of interest rate increases,” Lynch explains. “That means global interest rates will remain high, averaging around 4 percent over the next two years, roughly twice the average recorded during the two decades before the pandemic.”

Indermit Gill, the World Bank’s chief economist, specifically warned that “This is a major risk confronting the global economy — interest rates remaining higher for longer and an already weak growth outlook becoming weaker.”

Obviously, cutting interest rates isn’t the only thing we need to do in order to get rent and housing prices under control. As I wrote last week, we need to embrace a large suite of policy solutions to build millions of units of housing across the nation. But until interest rates are finally down to affordable levels, it’s going to be hard for developers to secure the funds to build those units in the first place—not to mention the fact that prospective homebuyers can’t afford the extra costs that sky-high mortgage rates are adding to the price of housing.

Let’s Talk About CEO Pay

Today, the results of a Tesla shareholder vote on a potential $46.9 billion compensation package for Tesla CEO Elon Musk will be revealed. (In fact, the results may already be public as you read this.) The package was overwhelmingly approved in 2018, but a Delaware Judge sided with shareholders who sued to stop the process, arguing that the pay was so high that it harmed shareholder value.

Due to the large figure at stake and Musk’s notoriety, this pay package has garnered a lot of attention over the last few weeks. Unfortunately, surprisingly few media outlets have given space over to some new measurements of CEO pay that offer remarkable transparency into the paychecks of the (mostly) men in the corner offices.

Jeff Sommer at the New York Times notes that four American CEOs raked in more than $150 million dollars each last year alone in traditional compensation—meaning flat payment, without stock holdings taken into account. But when you do consider how much CEOs are paid with stocks, as one new regulation does, those numbers rise much higher much faster.

“These new numbers — called compensation actually paid (CAP) — are often even bigger than the traditional chief executive payday bonanzas,” Sommer writes. “That’s the case for a man whose outsize pay is already a major issue for his company: Elon Musk of Tesla, who gained $1.4 billion in 2023 — more than any other C.E.O.”

Sommer writes that when you look at the highest-compensated CEOS in America, “The median pay for these executives — the midpoint, where half of the compensation packages are lower and half are higher — was more than $29 million.” At the same time, he adds, “we also know that the median pay of employees at these companies was around $100,000, and the median C.E.O.-to-worker pay ratio was about 300 to one.”

Remember that back in the 1970s, the average CEO-to-worker pay ratio was in the 20-to-one range. The difference between 20-to-one and 300-to-one is truly staggering, Sommer explains.

It means that for an average employee at one of these companies to earn as much as the C.E.O., she would have to transcend the human life span and toil for 300 years. And consider this: The American worker’s average annual wage in 2023 was only $65,470, according to the Bureau of Labor Statistics. At that wage, it would take 445 years to earn as much as the middle-of-the-road chief executive on this list.

And then we have to consider what these CEOs are doing in return for those gargantuan paychecks. Let’s look at a supposed American corporate success story: “John Deere reported a profit of over $10bn in fiscal year 2023 and its CEO John May received $26.7m in total compensation,” writes Michael Sainato at the Guardian. “John Deere spent over $7.2bn on stock buybacks in 2023 and provided shareholders with more than $1.4bn in dividends.”

In return for those record profits, sky-high executive compensation, and outsized shareholder value, John Deere is rewarding its factory workers with hundreds, maybe thousands, of layoffs this year. And the company is moving manufacturing plants to Mexico. Here’s a rule of thumb: The bigger the CEO paychecks are, the more inhumanely the corporation treats its workers.

All those big paydays are enough to give Sommer pause. “I suspect that the stock market would perform well even if C.E.O.s merely earned millions, instead of hundreds of millions, and rank-and-file workers got a bigger slice of the pie,” Sommer writes. “That’s not the way the world has been going, not for many years. But it doesn’t have to be that way,” he concludes.

That’s exactly right—this extractive world of billion-dollar executive payouts and shrinking worker pay is a policy choice. Specifically, it’s the result of 40+ years of trickle-down economics that concentrates wealth at the top of the income scale and forces everyone else to scramble to make a living. Just as trickle-downers rewrote the rules of the economy a half-century ago, so can middle-out economics rewrite the economic rules for the next century.

Will Kansas Embark on a Second Trickle-Down Experiment?

At Fast Company, Marcus Baram writes that as the federal government adopts more middle out economic policies, Republicans in state legislatures around the country are doubling-down on trickle-down economics by handing big tax breaks to the wealthiest few. He looks at Kansas, where the wealthiest man in the state, Charles Koch, has pushed a huge tax reduction bill through the state legislature.

“A bill that included a flat 5.25% personal income tax, an 8% reduction from the current rate for top earners, was approved by Republicans in both chambers, though critics say it would disproportionately benefit the wealthy in the state,” Baram writes. “The top 20% of earners in Kansas—those with average annual incomes above $315,000—would get nearly 40% of the benefits, with Koch himself receiving an estimated $485,000 in annual tax breaks under the proposal, according to the Institute on Taxation and Economic Policy, a nonpartisan research group that favors a progressive tax system. It would also cost the state almost $650 million every year once fully implemented, per ITEP.”

“Kansas is not the only state pushing for major tax reductions,” Baram writes. “Mississippi has fully succeeded in instituting its version of trickle-down economics, with Gov. Tate Reeves pushing two of the biggest income tax cuts in state history. Having won reelection last year, he’s now calling for lawmakers to completely eliminate the personal income tax—which makes up about one-third of state general fund revenue.”

But Kansas is especially noteworthy because it was the tip of the trickle-down spear in 2012 and 2013, with then-governor Sam Brownback slashing taxes for the wealthy so much that the state budget nearly collapsed, and Republicans had to roll back the cuts in order to avert a disaster. These latest tax cuts would again devastate Kansas’s public school system and punch an enormous hole in the budget.

This is like a funhouse mirror version of the Fight for $15, which saw cities and states embrace a higher minimum wage as other localities stood on the sidelines and watched. Once it became apparent both through casual observation and rigorous study that growing the wage was good for the local economy, with none of the job losses or out-of-control price increases threatened by the opposition actually materializing, we saw $15 minimum wages spread around the country. If Kansas does adopt this handout for the wealthy, it will serve as proof for other states and localities that the wealthy few aren’t the job creators, they’re the wealth extractors.

This Week in Middle Out

This is a great post to bookmark and share with friends who don’t pay close attention to politics: Vox has put together a review of the Biden Administration’s middle-out pro-consumer policies. Titled “Biden’s overlooked campaign to protect Americans from Big Business,” the post details everything from junk fee protections to cable bill transparency to breaking up Ticketmaster.

And here’s another big proposal from the Biden Administration that would change the lives of working Americans: A new rule banning the inclusion of medical debt in credit history. This will protect the credit ratings of millions of Americans who had medical emergencies and weren’t able to comparison-shop their treatment plans. The Consumer Financial Protection Bureau estimates that “15 million Americans still have $49 billion of medical debt that is hampering their scores.”

Scott Sowers at the Washington Post writes that the CFPB is also “expected to get tougher on regulating payday lenders and other firms that offer high-interest, short-term loans. This type of lending — which often targets low-income borrowers — has long drawn fire from consumer groups on grounds that these small-dollar loans quickly balloon when they’re not repaid, accruing exorbitant fees and interest.”

Unfortunately, it’s looking like some Senate Democrats might cross the aisle to vote down a Biden Administration regulation that establishes staffing minimums in nursing homes nationwide. “The standard would, among other things, require 33 minutes of care per patient per day from a registered nurse, which backers argue would make nursing homes safer and ensure seniors are not left in need for hours,” reports Axios. President Biden has said he would veto the bill if it makes it to his desk, so the staffing minimums are almost certain to stay in place.

A program to modernize and industrialize housing construction pioneered by HUD Secretary George Romney and the Nixon Administration in the 1970s has found great success in modern-day Sweden and Japan, reports the New York Times’s Amir Hamja. Though the plan was piloted and developed here in the US, Congress killed funding for the mass production of modular housing in 1976.

This Week on the Pitchfork Economics Podcast

In the last few years, we’ve seen the rejuvenation of several major government agencies, including the IRS and the Department of Transportation. But arguably, the most exciting transformation is in the Federal Trade Commission, which has transformed from a sleepy organization during the age of trickle-down into a dynamo of activity in the last few years, fighting monopolies and corporate mergers with renewed vigor. On this week’s episode of the Pitchfork Economics podcast, Elizabeth Wilkins, former Chief of Staff and Director of the Office of Policy and Planning at the FTC, explains the reasons behind that dramatic transformation, and why it matters that the government is out there protecting Americans from corporate malfeasance.

Closing Thoughts

Last week, Jared Bernstein, the head of President Biden’s Council of Economic Advisers, delivered a speech about the Biden Administration’s trade policy. Bernstein’s speech didn’t make a lot of headlines, but it was an important clarification of the Biden Administration’s ideals and goals when it comes to international trade.

Bernstein suggested that the stresses on global supply chains during the pandemic have revealed the flaws in our global distribution system. He characterized the moment as a wake-up call for the whole world, and a lesson that relying on a single global supply chain for any product was a disaster waiting to happen.

Bernstein also recognized that “Widely accepted economic research shows that the shock of the sharp increase in Chinese import penetration in the 2000s led to lasting damage in many American communities, especially those that lost manufacturing jobs and the factories that previously anchored their communities.” Unregulated free trade with a nation that can artificially lower prices by paying workers pennies an hour and slashing regulations is a sucker’s bet.

But international trade between partners is not just a net positive—it’s absolutely essential for a 21st century nation. One of Bernstein’s most important quotes about this is right up at the top of the speech: “Recognizing and taking action against the negative impacts of globalization does not imply rejecting globalization. A renewed, robust, worker-centered focus on industrial policy should not be conflated with reduced trade or less financial openness.”

Healthy international trade begins with a healthy economy at home. Bernstein talks up the Biden Administration's investments in semiconductors and the green economy as a central part of the new trade policy. Those investments are encouraging private enterprise to make their own investments.

“I’m hard pressed to recall seeing such a quick, deep reaction to a public policy, one that’s a lot more complicated than sending out checks or boosting unemployment benefits,” Bernstein said. Best of all, he explained that those investments are “worker-centered, targeting good jobs, often union jobs, with an emphasis on places that have been heretofore left behind, places that often are themselves transitioning from old to new sectors.” That’s why you see a staggering amount of factories slated to open in the Rust Belt and in other regions that have been on the losing end of the last three decades of globalization.

Bernstein also set out four informal principles for nations to consider when engaging in trade with partner nations:

“Our citizens are not only consumers. They are also workers and the quality of their lives depend in part on jobs with dignity that provide them with a fair share of the pie they’re helping to bake.”

“Fighting climate change requires significant government intervention and international cooperation.”

“Trade policy is not just economics. It’s political economics,” meaning that if you reward nations that engage in lowest-common-denominator policies that exploit workers and pollute the planet, you’ll get more of those anti-cooperative policies.

And lastly, “Unfair trade exists,” which means that there’s never a perfectly even playing field between trading nations.

With each passing week, the Biden Administration hones in on a trade philosophy that truly acknowledges the international realities of the world as it is in the first half of the 21st century. It’s a philosophy that rejects both the almost libertarian globalization of the late 1990s and early 2000s and the far-right nationalist tariff fights of the last decade, forging instead a more pragmatic understanding that puts people before corporations, and rejects a race to the bottom with a handful of winners and hundreds of millions of losers in favor of broadly shared prosperity.

Be kind. Be brave. Take good care of yourself and your loved ones.

Zach