Middle-Out, Ten Years Later

Middle-Out, Ten Years Later

The Pitch: Economic Update for March 21st, 2024

Friends,

Over a decade ago, an influential quarterly journal called Democracy Journal published a special issue titled “The Middle-Out Moment.” The editors explained that they collected pieces from a number of authors (including Civic Ventures founder Nick Hanauer) because “the time is ripe for progressives to take up ‘middle-out economics’ as the definitive retort to trickle-down economics.”

The editors helpfully explained in their note that “Middle-out economics contends that prosperity doesn’t trickle down from the top, but flows in a virtuous cycle from the middle out.” It was an idea that had received barely any attention in the mainstream at the time. This was when the Fight for $15 was just starting to gain strength, and trickle-down’s grip over politicians on the left and right hadn’t yet started to loosen.

Looking back on it, they were right that change was coming. But they were wrong that it arrived, and too hopeful about how quickly it would take for this new paradigm to take hold. It turns out there was still a lot of work to be done and a longer road ahead.

Yet you can’t deny that incredible progress has been made. President Biden has centered working Americans in his economic policies, proving with our nation’s first-in-the-world economic recovery from pandemic lockdowns that middle-out really does grow the economy for everyone. And just as importantly, he’s also using the biggest platform in the world to make a compelling case for middle-out economics in virtually every speech he gives, explaining that the economy grows from the middle out and the bottom up—not the top down, as trickle-down economics has argued for decades.

To commemorate this amazing progress, and to mark how far we’ve come since the original middle-out moment, Democracy has just published a new issue called “The Middle-Out Moment Is Here.” It’s another symposium featuring some of the best and brightest thinkers on middle-out economics, and every essay in the issue is worth your time.

“In the years since a middle-out moment was previously declared,” Nick and Civic Ventures fellow David Goldstein announce in the opening of the issue, “the science that informs middle-out economics has greatly advanced, the empirical data that support its policy prescriptions have accumulated, the narrative that can drive its widespread adoption has matured, the circumstances that make its paradigm shift possible have accelerated, and the political leadership necessary to replace an old economic story with the new has been asserted by a President committed to using the powers of his office to help rebuild the American middle class.”

Felicia Wong, the CEO and President of the Roosevelt Institute, explains in her essay how the Biden Administration has upturned decades of political thinking by shaping its infrastructure and green-energy policy to direct “public capital to invest in key industries, aiming to attract private funding” in order “to move resources toward publicly important sectors, like clean energy, that otherwise would suffer from market failure and not grow with sufficient scale, speed, or broad-based popular benefit.” For decades, our leaders and economists believed that government investments would scare away private investment, and the Biden Administration is debunking that foolish belief in real-time.

We’ve also finally gotten a glimpse of what truly middle-out international trade policy would look like, and it’s very different from the extractive policies that hollowed out the factories and farmland of middle America. Todd Tucker of the Roosevelt Institute digs into why trade policies that center workers both here and abroad create better outcomes for everyone.

The Economic Policy Institute’s Heidi Shierholz, who also served as Chief Economist at President Obama’s Department of Labor, celebrates the Biden Administration’s big wins on behalf of American workers and lays out a game plan to expand those wins in a potential second Biden term in office. “When the wages of the people who are the most likely to spend are not suppressed—when middle-out economic policies prevail and workers have the leverage to secure fair wages through unions, strong labor standards, and low unemployment—the result is wage-led economic growth,” Shierholz writes. “Middle-out economics is good for workers, good for their families, good for their communities, good for the broader economy, and good for the nation.”

After 40 years of trickle-down indoctrination convinced economists and many working Americans that government investments are wasteful spending, Stanford Professor of Economics Neale Mahoney and former Biden Administration economist Ronnie Chatterji explain why smart investments can make a huge, transformative difference in the lives of working Americans—and why that’s a role only government can fill.

Former Deputy Director of Biden’s National Economic Council Bharat Ramamurti tells the full story of how President Biden’s investments in the American people set the stage for our first-in-the-world recovery from the global pandemic, and how it helped fight the battle against inflation as well.

Meanwhile, Sandeep Vasheen of the Open Markets Institute shines a spotlight on the Biden Administration’s under-appreciated work combating monopolies and other consolidations of corporate power, and why it’s better for the whole economy when there’s more competition in the marketplace.

Former Biden Administration adviser Jennifer Harris shares lessons from the Inflation Reduction Act’s creation and implementation, and she makes a point that I have yet to see articulated in the mainstream political media: ”perhaps the most profound legacy of the IRA will be the way it has reframed the problem of climate change—away from a market failure to be remedied through an explicit price on emissions to instead a problem of politics, industrial organization, and technology.” She offers an optimistic understanding that climate change isn’t a necessary byproduct of capitalism—it’s a problem to be solved through a unique blend of private and public expertise.

And finally, former Obama adviser Tara McGuinness makes the case for why middle-out economics isn’t just a way to build a stronger economy or to promote economic growth—it’s also a more ethical, responsible, sustainable way forward that promotes unity, interconnectedness, and shared civic pride.

I urge you to read these pieces and share them widely. This issue of Democracy Journal serves as an important touchstone for progressives as they prepare for a pivotal election year. It’s a reminder that after 40 years of extractive policies that expanded income inequality to historic levels, there is a plan to repair and rebuild the American economy. What’s more, the plan is built on sound economic principles—and, most importantly, the plan is working. If you’ve been spending the last few weeks doomscrolling about polls and primaries on social media, this is the antidote for your depression, and the blueprint for how to keep marching forward, together, into the future.

The Latest Economic News and Updates

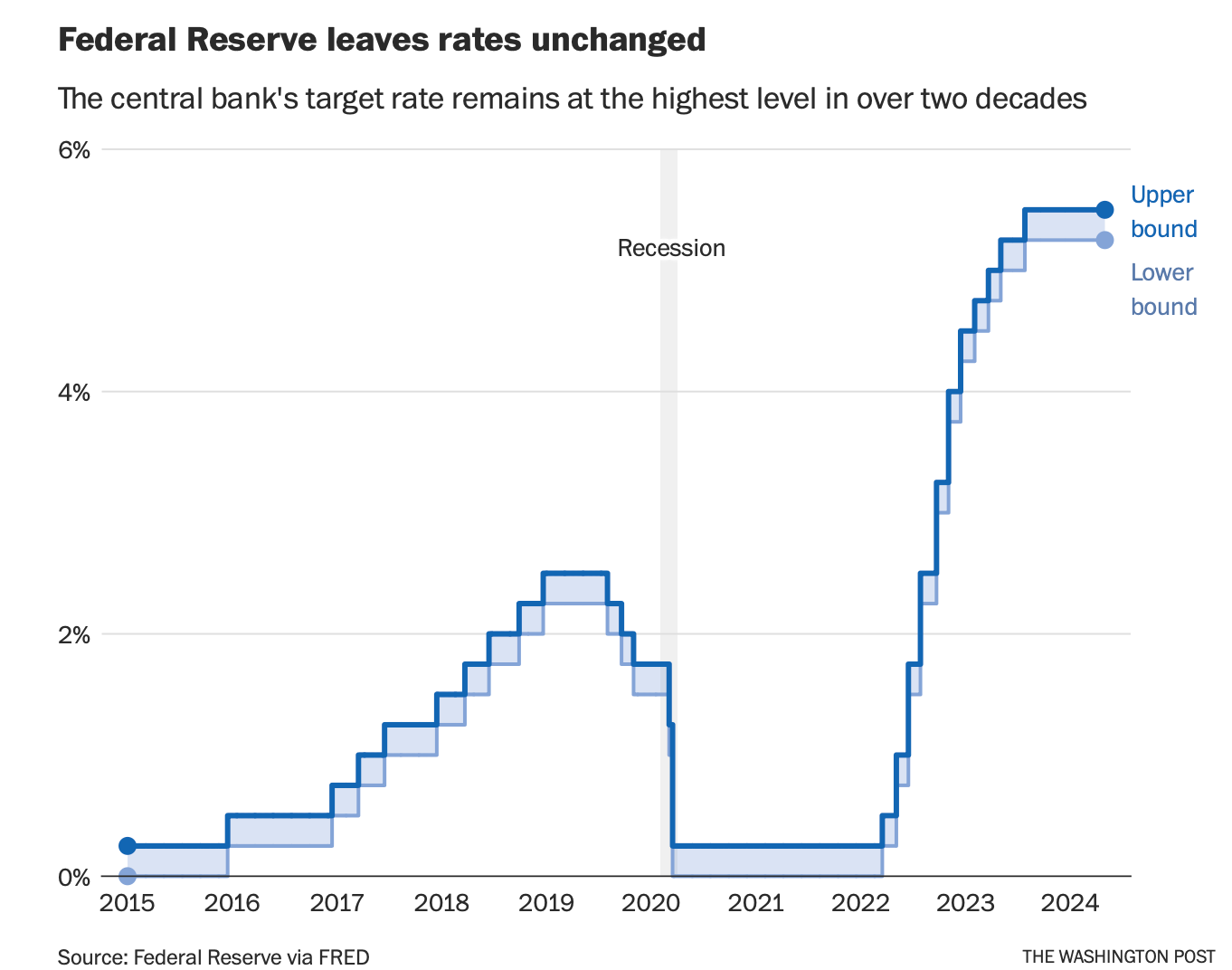

The Fed Stands Still as the World Keeps Spinning

“The Federal Reserve is still eyeing three interest rate cuts this year, as officials wait for a bit more confidence inflation is reliably falling to more normal levels,” writes Rachel Siegel at the Washington Post. “At the close of their two-day meeting on Wednesday, central bankers left the benchmark interest rate steady at between 5.25 and 5.5 percent. The move was highly expected and leaves borrowing costs at their highest level in 23 years.”

Even though inflation tipped up a bit last month, the Fed’s current economic predictions for the rest of the year remain strong: “Policymakers now think the economy will grow 2.1 percent this year, up from the 1.4 percent forecast in December. They also expect the unemployment rate will end the year at 4 percent, down slightly from previous estimates,” Siegel writes. That’s a pretty strong economic forecast—but then, the Fed’s predictions are anything but ironclad: Siegel notes that new economic projections are issued every few months.

The Fed’s inflation numbers are an imperfect tool—an aggregation of a large market basket of goods and services. Not every price is rising in lockstep, and many prices are falling fast. For the Post, David J. Lynch writes that the American market is being flooded with cheap Chinese products, and that could harm America’s recent manufacturing boom. “In February, U.S. imports from China cost 3.1 percent less than one year ago,” Lynch explains. “That helps the Federal Reserve’s fight against inflation. But those low-priced Chinese goods may cost American manufacturers sales, threatening the Biden administration’s election-year hopes of boosting the number of factory jobs.”

The trickle-down presidential administrations of the past would simply argue that the free market should determine the best products and the best price, taking a hands-off approach to American factory production. But President Biden’s administration is working from a middle-out economic understanding of the world, and that’s why yesterday the President made a big announcement: “The Biden administration is awarding up to $8.5 billion in grants and $11 billion in loans to tech giant Intel to support computer-chip production in several states, in one of the nation’s biggest ever investments in high-tech manufacturing seen as crucial to national and economic security,” writes Jeanne Whalen at the Post.

Under the trickle-down model, the free market is left to its own devices, which results in outsourced jobs as developing nations slash costs, wages, and safety standards to third-world levels. But the Biden Administration understands that big, targeted investments in high-wage, high-value sectors will eventually direct the market toward creating better outcomes for everyone. America doesn’t have to compete in every sector—we just need to invest in industries that create a better future, like green energy, technology, and other future-forward fields.

As Austin Goes, So Goes the American Housing Market?

For the Wall Street Journal, Will Parker writes about Austin, Texas, which has for the last decade-plus been ahead of the curve when it comes to housing. “Austin was at the forefront of the U.S. housing boom, when rock-bottom borrowing costs near the start of the pandemic fueled robust sales and sent home prices to new highs. Austin prices soared more than 60% from 2020 to the spring of 2022,” Parker explains.

Then, “A surge in interest rates crushed the housing market nationwide, and existing-home sales fell to a nearly 30-year low in 2023. Despite that collapse, home prices remain near record levels thanks to tight supply,” Parker writes, adding, “But in Austin, according to the Freddie Mac House Price Index, prices have fallen more than 11% since peaking in 2022, the biggest drop of any metro area in the country.” Austin’s rents have fallen 7% in the past year—more than any other American city.

But as you can see, Austin is still a lot more expensive than it was before the pandemic. And while the national average home price is considerably lower than Austin, housing prices in general went through an exceptional increase over the last four years:

President Biden offered a plan to lower housing costs in a speech this week, with programs including mortgage relief and lowering closing costs for homeowners, cracking down on rental junk fees and combating rent-gouging for renters, and encouraging the construction of more homes through tax credits and increasing banks’ contributions to the construction of affordable housing.

Thankfully, a recent court settlement ensured that home buyers are about to be relieved from one particularly onerous expense of buying a home. The National Association of Realtors paid a huge settlement in a court case that alleged realtors had been colluding to inflate their commissions for decades.

“Until now, home sellers paid about 6 percent of the sale price toward a fee that would be split between their own agent and the buyer’s agent,” writes Vox’s Whizy Kim. “Experts are divided on exactly how much impact this will have on home buyers, who will now likely have to start paying their agents themselves. The median sale price of homes as of late 2023 was about $417,700 — 6 percent of that amounts to a little over $25,000.”

It’s unclear now exactly what this settlement will do to home prices, but most experts predict that now that realtors will have to actually compete to offer better rates, we’ll see homebuyers’ expenses drop at least a little now that the standard 6% fee has finally been unwound.

The Battle for the Future of Retirement

Workers filed for a unionization vote at a Tennessee Volkswagen auto plant, marking the next big step in the United Auto Workers union’s campaign to build on last year’s successes. Those Tennessee workers would be wise to vote to join UAW, because a new study from the Center for American Progress shows that “Union households possess 1.7 times the median wealth of nonunion households.“

Additionally, the study finds that “The median wealth of union households is greater than that of nonunion households across every education level,” and that “Union membership closes the wealth gap between working-class and college-educated households.”

Union members, the study finds, are also more likely to own a house and have a retirement plan in place than their non-union counterparts.

And about those retirement plans: Peter Coy at the New York Times reports that he’s changed his mind when it comes to extending the retirement age. While he used to believe that Americans should work longer into old age as life expectancy grows, Coy now realizes that most people who work past retirement age are doing so because they have no choice but to work, and that they’re working in low-paying, low-quality jobs.

“One in eight people with no financial plan die without ever having retired. Far fewer people die without retiring if they have a defined-contribution plan, such as a 401(k),” Coy says. “Even fewer die without retiring if they have a defined-benefit plan, which is an old-fashioned pension in which the employer sets money aside for you based on your pay and job tenure.”

Coy now believes that there is a need for a government-run retirement savings plan. “Because it would require contributions from employees (in addition to the federal government for below-median-income workers), it would be a new form of induced savings. The government match portion couldn’t be tapped for anything but retirement,” he explains.

This conversation is important, because Republican presidential candidate Donald Trump, in a shocking reversal from his 2016 campaign, opened the door for Social Security cuts in a potential second term. Paul Krugman, in his latest column, explained why Trump’s calls to cut Medicare and Social Security should be taken seriously. “Biden has a clear plan to preserve these programs; Trump, wittingly or unwittingly, would probably help wreck them,” Krugman concludes.

Why Did Joann Fabrics File for Bankruptcy?

Earlier this week, you likely saw one or a few of these headlines about retailer Joann Fabrics filing for bankruptcy in the business section of your favorite news source:

Joann files for bankruptcy as consumers pull back on nonessentials

Crafts retailer Joann files for Chapter 11 bankruptcy as consumers cut back on pandemic-era hobbies

Joann files for bankruptcy amid consumer pullback, but plans to keep stores open

If you were just to scan the headlines, you’d think that the collapse of the eight-decade-old craft retail chain came because Americans are no longer pursuing their pandemic-era hobbies.

But it’s not that simple.

You have to go all the way to the bottom of the New York Times’s story about Joann’s bankruptcy to find a hint of why the chain is really in trouble: “The private equity firm Leonard Green & Partners bought Joann for roughly $1.6 billion in 2011, and spun it off publicly in 2021. Joann’s stock price initially climbed, but it began to tumble a few months later, and now trades for about 20 cents a share.”

Yes, it’s our old friend private-equity again, extracting value and pumping massive debt into brands that have lost some of their shine. Here’s a story from 2021, when Joann went public:

In past years, Joann’s sponsors pulled $5 million a year out of the company in the form of management fees. The fees continued even as the company’s debt made its way onto Fitch’s “Loans of Concern” list….Those management payments, which are set to stop after the IPO, are dwarfed by the company’s interest expenses, which in past years have topped $100 million. As of October, the company’s long-term debt stood at $921.6 million, down from a peak of $1.3 billion in 2019, after Joann repurchased $347.1 million of its term loan debt at prices below its original face value.

Stop me if you’ve heard this story before: A private equity firm buys a trusted long-time retailer, pumps it full of debt, takes it public, and then basically keeps it limping along after bankruptcy, presumably until it comes time to finally sell the parts for scrap. That’s a compelling story about a pernicious practice that’s happening all the time in America today, but most mainstream news sources simply choose to repeat the press-release copy about pandemic-era hobbies dying out, instead. Without the media making clear connections between the true cause-and-effect of private equity, we’ll be doomed to repeat this wasteful pump-and-dump cycle for years to come.

This Week in Middle Out

“The Biden administration announced Friday it is looking to take action against junk fees for college students and student loan borrowers,” writes Lexi Lonas in The Hill. “The White House said it is targeting four kinds of junk fees in its initiative: student loan origination ones, college banking junk fees, automatic charges for textbooks, and colleges keeping leftover money in a student’s meal plan.”

The Biden Administration “will require automakers to ramp up sales of electric vehicles while slashing carbon emissions from gasoline-powered models, which account for about one-fifth of America’s contribution to global warming,” writes Maxine Joselow in the Washington Post.

This Washington Center for Equitable Growth study explains why anti-competitive consolidation is such a huge problem in the health care sector, and proposes policies to stop hospitals and health care systems from buying each other up.

Robert Kuttner at the American Prospect explains why President Biden’s action to stop the sale of US Steel to Japan’s Nippon Steel is a pro-union, pro-worker “commitment to rebuild domestic industry,” as well as a “rejection of corporate-driven ‘free trade’” that has hollowed-out American industries over the past 40 years.

And the Center on Budget and Policy Priorities explains how the Affordable Care Act has improved outcomes for Americans, cutting the rate of uninsured Americans roughly in half over the past ten years.

The Center for American Progress offers some ideas to cut wasteful overspending on Medicare Advantage programs by anywhere from 20 to 30 percent annually, which could save anywhere from $1.3 and $2 trillion dollars that otherwise largely would have gone to insurance company profit margins over the next decade.

For CNN, Naomi Walker and Amy Hanauer—no relation to Nick—explain how reforming the estate tax would help to rebalance the tax code and combat wealth inequality. “Senator Bernie Sanders and cosponsors seek to restore the estate tax exemption to $3.5 million per spouse, which would still shield all but 0.5% of estates from the tax. Additionally, President Joe Biden’s budget proposes closing some of the estate tax loopholes,” the write. “Doing so would raise real money. The official revenue estimators have said that Sanders’ proposal would raise roughly $400 billion over a decade, which is twice what we’d need to provide paid family leave to all American workers to care for a new baby or a sick family member.”

This Week on the Pitchfork Economics Podcast

At the State of the Union speech this month, President Biden suggested that he was preparing to finally apply his middle-out economic policies to the tax code by ensuring that the wealthiest Americans pay at least as much as the people who work for them. But before he can unrig the tax code, he has to deal with the mess that his predecessor left. On this week’s episode of the Pitchfork Economics podcast, Samantha Jacoby, senior tax analyst at the Center on Budget and Policy Priorities, explains that the tax policies enacted by former President Trump in 2017 functioned as a multi-hundred-billion-dollar handout to the most powerful corporations and wealthiest Americans. Many of Trump’s tax policies are on the verge of expiring, and the next election will choose the Congress that decides which tax plan—Trump’s or Biden’s—will shape the nation for the next decade. Jacoby walks Nick and Goldy through the true cost of Trump’s tax plan, and what Biden’s tax plan might mean for the economy.

Closing Thoughts

Sometimes, if you’re lucky enough, you get to watch an idea break into the mainstream as it happens. That’s what it felt like reading Jennifer Rubin’s editorial for the Washington Post last week. I have to include a shot of the headline because it feels so revelatory to read it in the Post’s headline font:

If for whatever reason you can’t read the above screenshot, the headline reads “‘Trickle-down economics’ is a scam that ignores decades of evidence.” We at Civic Ventures literally couldn’t have put it better ourselves.

Rubin cites several major pieces of research arguing that tax cuts for the rich do not result in shared economic prosperity. For example, one British study of 18 nations over 50 years, some of which did cut taxes on the rich and some of which didn’t, found that “per capita gross domestic product and unemployment rates were nearly identical after five years in countries that slashed taxes on the rich and in those that didn’t, the study found.”

The big difference between those nations was that “incomes of the rich grew much faster in countries where tax rates were lowered. Instead of trickling down to the middle class, tax cuts for the rich may not accomplish much more than help the rich keep more of their riches and exacerbate income inequality.”

Another study Rubin quotes in the piece finds “strong evidence that cutting taxes on the rich increases income inequality but has no effect on growth or unemployment.”

Readers of this newsletter are familiar with these findings. But it is still validating and energizing to see these facts repeated under the banner of one of the nation’s largest newspapers, backed up with plenty of convincing evidence, and crystal-clear in its messaging. Just get a load of Rubin’s closing paragraph:

“Trickle-down economics is a scam. Renewing tax cuts for the rich that are due to expire at the end of 2025 would do about as much for you as a degree from Trump University.”

It’s attention-grabbing, it’s opinionated, and it also happens to be true. Editorial writing at its absolute best.

Be kind. Be brave. Take good care of yourself and your loved ones.

Zach